Last week’s framing was unusually clean: Oil was the variable, and 73–74k was the reclaim. The premise was that BTC can stabilise quickly after geopolitical shocks unless the shock becomes an oil/inflation event that tightens financial conditions.

That caveat immediately became the base case. Instead of the usual “geopolitics shock → quick mean reversion,” the market got something else entirely: a multi-day energy shock that bled into rates, volatility, and ultimately the crypto risk complex through the inflation channel. Oil’s path mattered more than the first candle exactly as flagged. On the tape, BTC did what fragile ranges do in headline regimes: it tagged the reclaim zone intraday, but it did not hold it into the end of week.

BTC trading back above 74,000 on March 4, confirming the reclaim attempt. But by Friday’s risk-off close, Reuters had BTC back down near 68,141, while ETH was ~1,979 with oil simultaneously printing its biggest one-day spike in years.

The Energy Shock

The week’s core macro fact was not “risk sold off.” It was energy prices repricing higher, fast, in a way that pulls inflation back into the conversation and forces markets to stare at the central-bank reaction function again.

First, energy markets began pricing in disruption risk with the Strait of Hormuz effectively closed, and tanker transits collapsing (Vortexa data: four crude tankers transited on March 1 versus a 24/day average since January).

Then the “risk premium” moved from theory to settlement prices. On Friday, WTI settling at $90.90 (+12.21% on the day) and Brent at $92.69 (+8.52%), with WTI’s day move noted as its biggest one-day gain since 2020.

The reason this mattered globally is mechanical: the Strait is not a marginal route. The U.S. Energy Information Administration estimates that in 2024 oil flows through Hormuz averaged about 20 million b/d, roughly 20% of global petroleum liquids consumption OPEC+ did respond, but the scale mismatch was the story. OPEC+ agreed a 206,000 bpd April output increase, meaningful as a signal, not as an offset to severe transport disruption through a chokepoint.

As pointed out by Kobeissi: “…our models show US CPI inflation rising to 3.2% if current oil prices are sustained. A move to $110/barrel opens for 3.5% CPI, and $130/barrel opens for 3.9%.”

Not a great sign for risk on assets.

Macro

The phrase that best described cross-asset behaviour this week was: inflation risk re-entered the room, and suddenly the usual hedges stopped behaving like hedges.

As investors searched for safety, traditional refuges moved unpredictably: the dollar held up better than many alternatives, while sovereign bonds struggled to attract classic safe-haven flows because traders were pricing them primarily on the inflation outlook rather than defence properties.

Rates markets responded accordingly. Global government bond markets as suffering one of their worst weekly losses in months, driven by concerns that war-driven energy inflation could force less dovish central-bank paths. The pressure was especially notable in the front end (2-year sector) across the U.S., UK, and Germany.

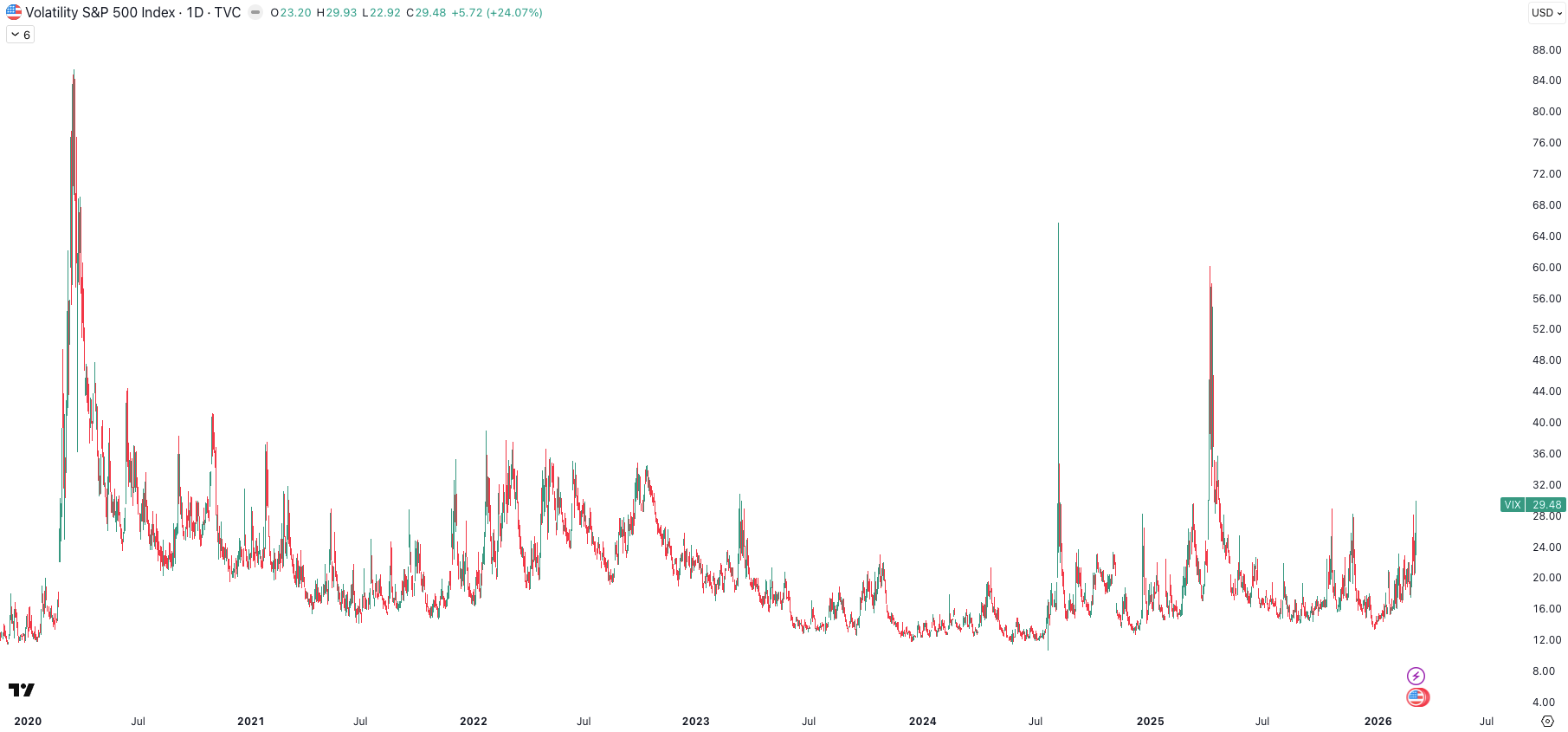

Equity volatility followed energy higher. VIX closing at 29.49 on Friday, its highest close since late April, while the S&P 500 logged its biggest weekly percentage decline since mid-October (down 2.02%), and the Dow saw its biggest weekly loss since early April (down 3.01%).

The macro calendar did not help because it introduced a second, conflicting impulse: growth wobble signs. On Friday, U.S. nonfarm payrolls declined by 92,000 in February and the unemployment rate rose to 4.4%, while emphasising that weather and a healthcare strike contributed to noise, but that the combination of weaker labour data and rising oil prices puts the Fed in a difficult spot.

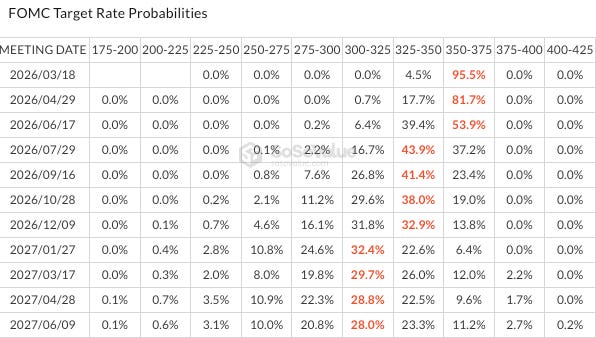

That brings us to the key macro gate for the coming week: CPI. The U.S. Bureau of Labor Statistics schedule shows February 2026 CPI is released March 11 at 08:30 ET. Market is expecting +0.2% m/m CPI for February, while also noting markets may discount a “tame” print because it largely predates the conflict-driven energy spike, yet an upside surprise would still be toxic for risk because it would compound inflation expectations. In terms of pricing, market is expecting no cut from Fed until Q3 2026.

Crypto

From a pure crypto-technical perspective, the week can be summarised in one sentence: the market attempted a reclaim and got rejected, which is exactly why reclaim levels matter more than bounces.

Last week’s note described 73–74k as the clean line in the sand, with the logic that reclaiming it would flip the late-February structure from lower highs into something that can sustain higher lows; failing to reclaim keeps the tape in “repair mode” rather than trend continuation.

This week delivered the “failure” branch of that decision tree:

A reclaim attempt happened. BTC broke back above 73k on March 4

The attempt did not survive the energy/rates reprise into Friday. BTC sold off to at ~68,141 on March 6 as oil spiked and equities sold off.

The weekend did not repair it. BTC closing ~66,905 on March 8.

ETH remained in the “damage control” bucket. Last week’s note called it a defence phase, arguing that any bounce below 2,200 is still relief unless structure rebuilds. This weeks price action, consistent with that thesis: it is not reclaiming, it is stabilising below broken levels.

One important nuance: the market still tried to trade local crypto catalysts. The rally into March 4 coincided with renewed focus on the CLARITY Act and clearer “rules of the road” narratives. BTC surging toward $74k after Donald Trump endorsed the bill with short term tailwind for crypto equities.

But the crypto-policy impulse faded because the legislation itself re-entered the grinder. Talks hit a new impasse as banks rejected a White House-backed compromise, with the dispute centred on stablecoin-linked rewards/yield and deposit-flight risks. In other words: crypto tried to rally on idiosyncratic news, but macro (oil → inflation) still overpowered it.

Prediction Markets & Price Discovery

One of the most interesting developments this week came from crypto markets themselves. While traditional markets were closed, Hyperliquid’s oil market continued trading, briefly pricing crude above $110.

The conflict has been traded not only through crude futures and defence equities, but also through 24/7 crypto-native instruments:

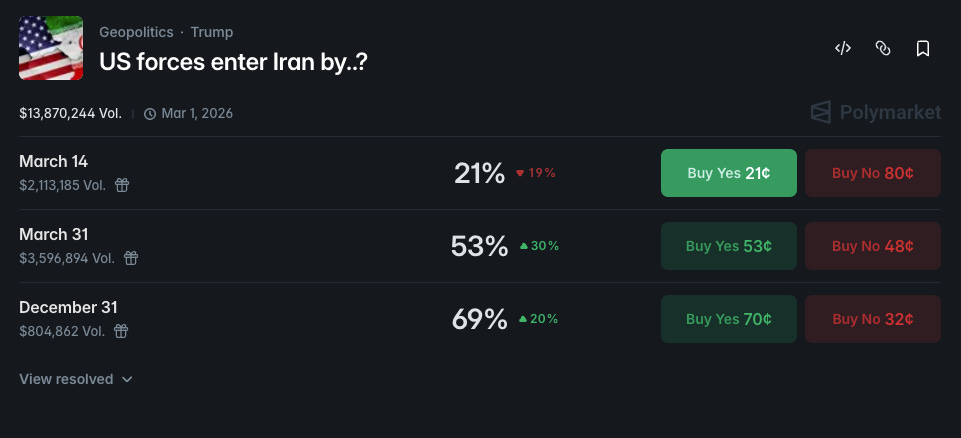

Polymarket’s “US forces enter Iran by..?” contract shows total trading volume around $13.9m, illustrating that the geopolitical tape has been continuously priced during off-hours.

Hyperliquid has become a visible venue for weekend commodity price discovery via oil-linked perpetuals. Oil-linked perps on Hyperliquid surging after the initial strike news (late February), explicitly framing the venue as part of the market’s real-time reaction function. As market stays closed on the weekend, hyperliquid USOIL is indicating a potential opening price at 116.

Historically, crypto has often reacted first to macro shocks simply because it trades continuously. Now that synthetic commodities are trading on-chain, the signal could become even stronger. It will be worth watching how closely Sunday crypto pricing aligns with Monday commodity futures going forward.

If these markets begin anticipating macro moves consistently, they could become an important information source.

The Week Ahead

The baseline assumption remains uncomfortable but straightforward: the surface area of the conflict is expanding, which means headline risk cannot be treated as background noise. Markets are now operating in a regime where geopolitics can directly drive macro variables, and those macro variables then transmit into risk assets.

The tactical framework for the week ahead can still be reduced to a three-gate checklist, although one variable clearly dominates the others.

I. Oil is still the variable.

Shipping disruption through the Strait of Hormuz has been documented as severe, and oil has already repriced sharply higher. If oil stabilises, history suggests BTC is more likely to stabilise and mean-revert. If oil trends structurally higher, BTC’s recovery profile tends to flatten, because the trade becomes “inflation shock” rather than “geopolitics shock.”

II. BTC structure is still the gate.

73–74k remains the key level. This week proved why: the market reclaimed it intraday and then rejected it into the weekend. Until that zone is reclaimed and held, rallies are best treated as repair/short-covering rather than trend resumption.

III.CPI is the next macro catalyst, but it is a backward-looking print.

The U.S. Bureau of Labor Statistics release is March 11 (08:30 ET). Markets care less about “what February inflation was” and more about “what the oil shock means for March/April inflation expectations,” which is why even a benign print may not be enough to stabilise risk if oil keeps squeezing.

Ultimately, this remains a headline-driven tape. Energy and by extension crypto is not a purely technical market in this regime. Every strike report, convoy update, policy statement, and diplomatic signal can force discontinuous repricing and the existence of 24/7 crypto-native venues (perps + prediction markets) compresses reaction time further.