In last week’s, Insider - The Bounce needs flow, we argued that crypto was in a bottoming process, not in an all-clear. That remains the right frame. The bounce never really earned the right to become a trend, and this week the missing ingredient became even more obvious: flows. The rebound needed confirmation from institutional buying. Instead, the market got another spell of ETF selling, another reminder that macro is still tight, and more evidence that Strategy’s capital structure remains one of the biggest overhangs in the asset class.

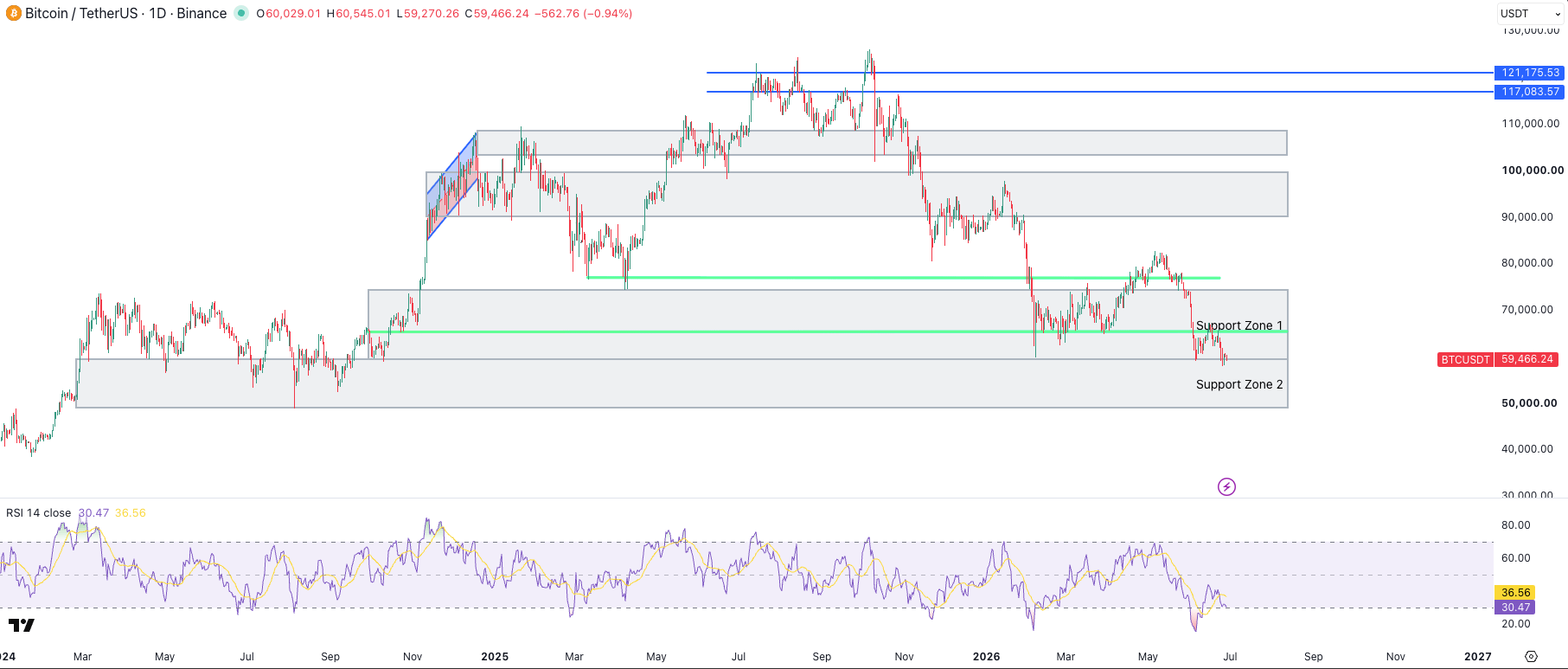

The result is that the market feels closer to a low than it did a fortnight ago, but not cleaner. Bitcoin is hovering around the $60,000 area after extending its 2026 drawdown, while broader risk appetite remains highly selective. BTC finished the week -7.1%, ETH -9.7% and SOL -3.8%. This is not the indiscriminate risk-off of a panic, nor is it the broad-based sponsorship you want to see at the beginning of a fresh crypto up-leg. It is a market still trying to absorb forced selling, tighter financial conditions and a funding squeeze in one of its most important bellwethers.

Crypto

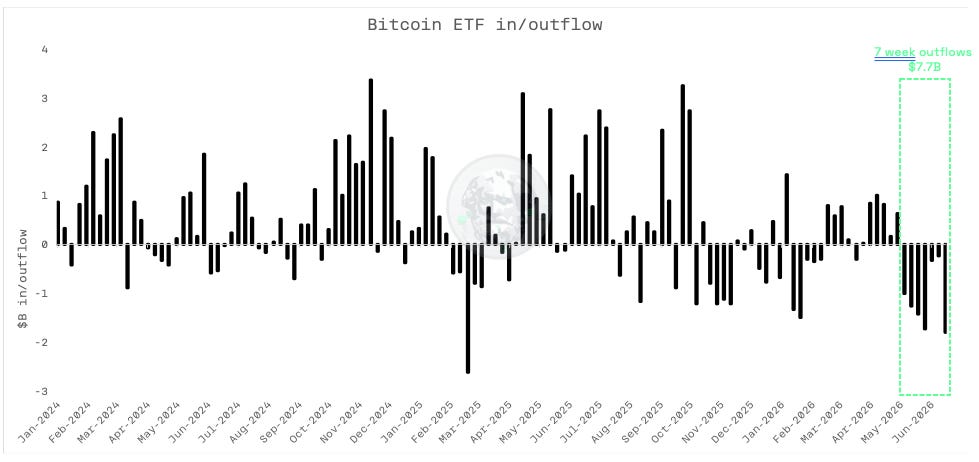

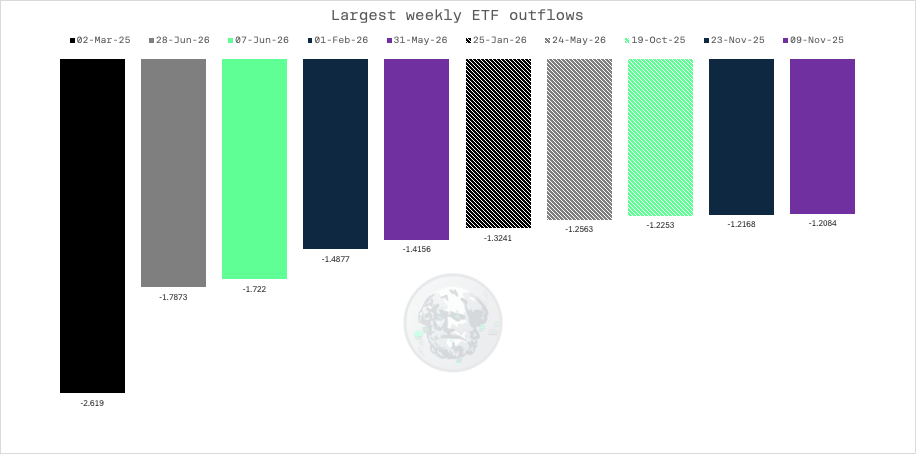

Flows remain the missing confirmation. Since inception BTC ETF has now had 7 weeks of consecutive outflows, with last week alone being the second biggest in its history of -$1.78B.

Within the top 5 the last 7 weeks has manage to take the top 3 stops and cummulatively this 7 week window has led to over $7.7B of outflows. That is not just a sentiment indicator. It tells you institutional sponsorship has not returned in size, and in a market like this that means every other overhang matters more. When the ETF complex is absorbing redemptions instead of fresh inflows, price becomes more vulnerable to treasury de-risking, cross-asset reallocations and funding stress elsewhere in the ecosystem.

That is why we still do not think the sell-off is over. The market may be close enough to a local low to produce sharp squeezes, but a durable low usually comes with either a clear macro easing impulse or a visible return of sponsorship.

We have neither. The tape has become oversold enough for rebounds, the market may be trying to form an early accumulation structure near the high-$50,000s, but it has not yet produced the kind of sign of strength that usually confirms the range is changing character. For now, it still looks more like an attempted base than a completed one.

That also fits the broader intermarket picture. Crypto is no longer trading as a self-contained narrative asset. It is trading as a flow-sensitive, macro-sensitive risk asset that competes directly with the AI complex for capital. Semiconductor ETFs have absorbed more than $21 billion of year-to-date inflows while bitcoin ETFs have been bleeding capital. That helps explain why crypto can look cheap on its own chart and still fail to rally: it is not enough for something to be oversold if capital is still rotating aggressively elsewhere.

The more constructive read is relative value. TOTALES (Total crypto market ex stablecoins) vs Nasdaq is now close enough to long-term support that the asymmetry is improving. Not yet a trigger, not yet a conviction trade, but a level worth respecting. If that ratio begins to stabilise while ETF selling slows, crypto-versus-AI rotation becomes a serious conversation rather than a theoretical one.

Macro

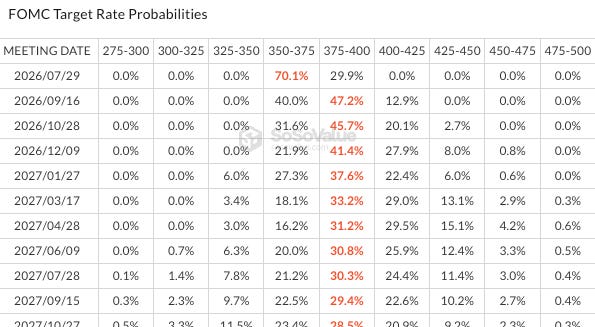

Macro still sits on top of the stack. The Federal Reserve held rates at 3.50%–3.75% in June, but the message markets heard was unambiguously hawkish.

May payrolls increased by 172,000

Unemployment held at 4.3%

Retail sales rose 0.9%

First-quarter GDP was revised up to 2.1%

Weekly jobless claims fell to 215,000.

At the same time, the Fed’s preferred inflation gauge rose 4.1% year on year in May, with core PCE at 3.4%. That is not a recessionary mix, and it is not weak enough to force the Fed into comfort. It is a combination that leaves policy restrictive and keeps rate-hike risk alive.

The market’s reaction has been meaningful. Currently pricing in a 30% chance of a rate hike in July, but higher probability of hikes in Q3/Q4.

A Reuters poll of economists, however, still found the modal base case was no further hikes in 2026. That gap is important. It means financial conditions have tightened more through communication and repricing than through realised policy. In effect, the market is doing some of the tightening for the Fed.

We do not believe the current degree of hawkishness is necessarily durable. The markets have rewarded Warsh’s inflation posture, with long-term break-evens falling sharply since mid-May. But if inflation starts to fall, and especially if the energy impulse continues to fade, we suspect the tone to soften. The simple point is that the market is still acting as if second-round inflation effects are the main danger. Our bias is that once first-round energy effects fade, the appetite to keep talking like a hawk will fade with them.

There is a useful historical analogy here. Reuters’ review of Powell’s tenure reminded markets that Powell’s October 2018 “long way from neutral” remark tightened conditions sharply, before he pivoted weeks later to saying rates were “just below” neutral. New Fed chairs do sometimes feel the need to establish anti-inflation credibility early. When conditions tighten fast enough, that posture can change quickly. That does not mean Warsh is about to turn dovish. It does mean the market may be extrapolating too much from the first act of a new chairmanship.

There is another reason the long end still matters even if the front end stabilises: AI financing demand. SpaceX sold $25 billion of bonds after generating an order book of roughly $85 billion, while the BIS warned that debt-funded AI investment and fragility in core bond markets are becoming more tightly linked. That matters for crypto because even a softer oil tape does not automatically deliver easier long-end conditions if a huge capital-spending cycle is competing for debt-market capacity at the same time. In other words, macro relief can arrive more slowly than bulls expect.

Strategy and STRC

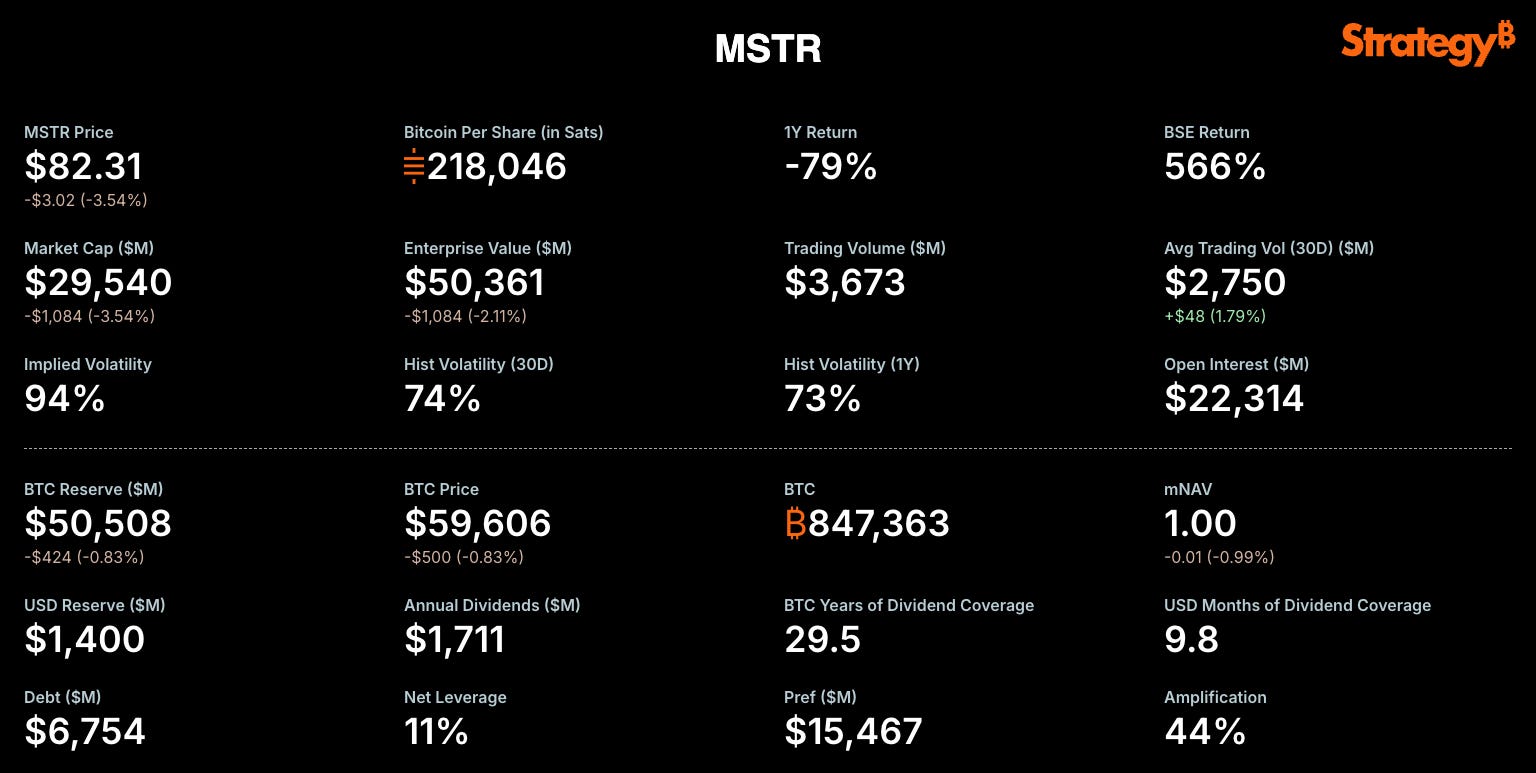

The deeper crypto-specific overhang is still Strategy. The company remains the largest corporate holder of bitcoin and has continued to buy selectively, with holdings reaching 847,363 BTC by late June. But the market is no longer focused only on the size of the bitcoin stack. It is focused on the cost and durability of the capital structure funding that stack.

That is why STRC matters so much, which closed at $74 on Friday, well below its $100 target trading level, sending the effective yield into the low- to mid-teens.

Another step-up in the dividend rate is likely, from 11.5% to at least 11.75%, and potentially higher if pricing remains weak, on about $10.5 billion outstanding. The current annual preferred dividends is at around $1.7 billion. That is not a side plot. That is the cost of capital story now sitting on top of the bitcoin story.

What Strategy has done in response is revealing. The company has continued to issue common equity, but the latest fundraising was used far more to rebuild cash reserves than to add meaningfully to BTC. Around $300 million of recent issuance went into the reserve, taking cash to roughly $1.4 billion. That tells you management is prioritising liquidity and optionality. Rationally, that makes sense. But for the market it changes the read-through. Strategy is not currently functioning like a relentless marginal buyer. It is functioning like a levered bitcoin treasury trying to protect the plumbing of its own funding model.

This is why we think bitcoin will struggle to print a durable low until there is greater clarity around Strategy and its BTC. A forced sale is not our base case today. The balance sheet is not there yet. But the market is trying to price the path by which one could become conceivable: the common loses more of its premium, the preferred remains below par, issuing more common becomes increasingly dilutive, bitcoin purchases shrink further, and any renewed pressure on reserves or redemptions raises the spectre of BTC monetisation. Whether that ends in an actual sale or merely in the fear of one, it is the overhang that still needs to clear.

That is also why a genuine capitulation event linked to Strategy could be the type of washout that finally produces a cleaner low. Not because it would be healthy, but because it would resolve uncertainty. Markets often bottom not when news becomes good, but when the largest unresolved risk becomes concrete enough to discount fully.

Bottom line

The message this week is simpler than the tape. The market is trying to build a low, but it has not yet earned the right to trend. ETF flows remain poor, macro remains restrictive, and the Strategy overhang remains unresolved. That is enough to keep us cautious even though positioning, sentiment and price all look much more washed out than they did earlier in the month.

The constructive case is not hard to see. Warsh may not stay this hawkish if inflation rolls over. Oil has already shown it can fall quickly on any genuine easing in Middle East tensions. Relative crypto-versus-tech valuations are becoming more interesting. And BTC itself is close enough to major support that the downside from here is more asymmetrically two-sided than it was from much higher levels.

But that is not the same as a clean bottom. For that call to improve materially, we would want to see outflows stop, the Fed’s effective hawkishness fade, the long end calm, and evidence that the STRC problem is being solved rather than merely financed around. Until then, the right posture is still the same as last week: respect the bounce when it comes, stay alert to relative-value opportunities, but do not confuse a technical reversal with cleared downside.