In last weeks The Insider - Technical Reversal, we said the market was in a bottoming process, not an all-clear. That is still the right frame. The bounce arrived exactly where it should have: after a washout, after positioning got cleaned up, and after one of the market’s biggest overhangs, Strategy’s willingness to sell bitcoin, stopped deteriorating. But the key word is still process. This week gave us relief, not resolution. Crypto found support, oil briefly backed off on hopes of a U.S.-Iran deal, and Treasury yields eased for a moment, but the Federal Reserve then pulled the macro floor away again by keeping rates at 3.50%-3.75% and signalling that hikes, not cuts, are the relevant tail risk for the remainder of 2026.

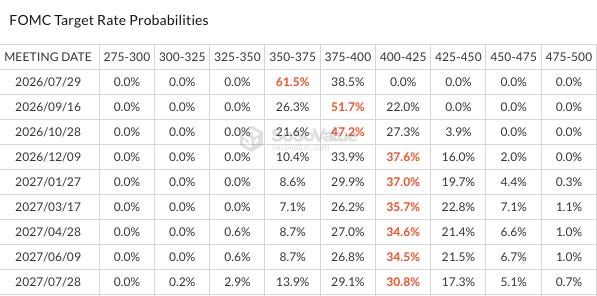

That matters because the market has repriced the Fed higher. After the June meeting, futures shifted towards a meaningful chance of a hike by October and a still larger probability by December, while Warsh also launched a review of Fed communications that investors fear could reduce forward guidance and push term premia higher. In other words, even if headline oil prints cool for a few sessions, financial conditions are not cleanly easing. They are becoming more conditional, more volatile and more dependent on the long end.

Crypto

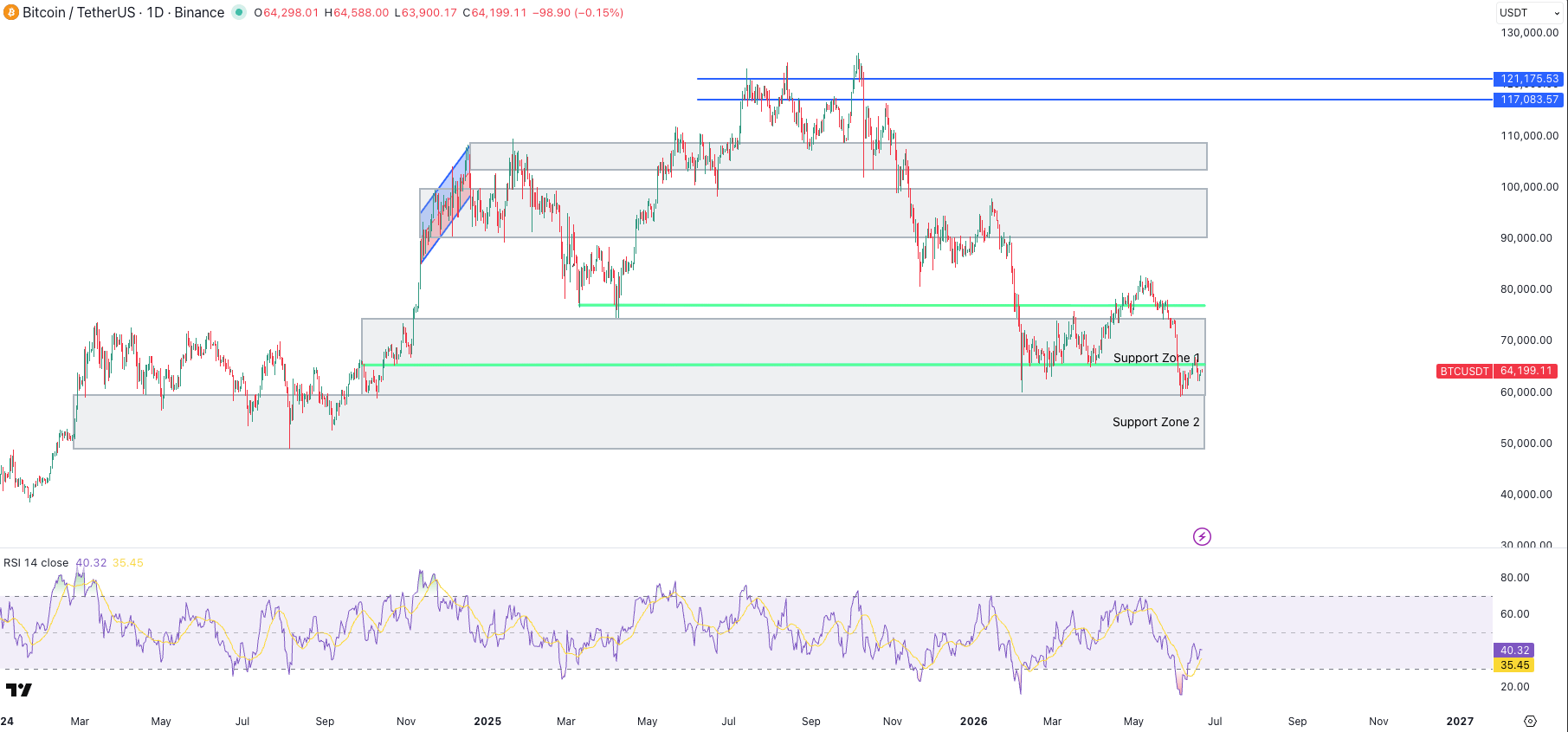

BTC traded like a market trying to bounce before it has earned the right to trend. Early in the week the tape improved as news of a U.S.-Iran framework deal and a drop in oil lifted risk appetite, pushing bitcoin back into the mid-$66k area and briefly above $67k intraday. But that move faded as traders turned their attention back to the Fed, weak institutional sponsorship and the reality that a hawkish policy surprise is still a stronger driver of crypto multiples than one good geopolitical headline. By end of the week we closed around 64k.

The BTC structure remains a rebound inside a damaged range, not a repaired trend.

Likewise, on the broader tape, the TOTALES, Total Market cap ex-stables, looks like a market leaning on structural support rather than launching into fresh impulse. The setup is better than it was at the panic lows, but it still resembles a technical reversal more than a final low. The market has become less fragile, but it has not become safe.

Flows are the missing confirmation. Bitcoin ETFs continued to bleed this week and have now posted six consecutive weeks of net outflows, the longest stretch since inception with total outflow of $5.9B. The pace is slowing, which matters, as capital rotations has shifted towards specualtive capital in AI and megacap equity stories. We have enough for a tradable bounce: support held, momentum is oversold, and forced selling looks less aggressive. What we do not yet have is the kind of sustained flow recovery that normally sits underneath a fresh uptrend. Until ETF outflows stop and turn back into consistent inflows, the bounce is real, but still unconfirmed.

Strategy helped at the margin, but only at the margin. After unnerving the market with its earlier bitcoin sale, the company disclosed that it had bought 1,550 BTC for about $101.3 million at an average price of $65,332, bringing holdings to 845,256 BTC, while also increasing cash reserves to $1 billion. That removed the immediate fear that the company had become a persistent marginal seller into weakness. But the size of the purchase was small by Strategy’s own recent standards, and it did not change the bigger story: Strategy is now managing capital structure stress as much as it is managing bitcoin accumulation.

Macro

Macro was supposed to get easier last week. The script was straightforward: a softer oil tape after the U.S.-Iran framework, weaker inflation impulse, lower long yields, a calmer Fed and some breathing room for crypto. Instead, we got the first half of that script for about forty-eight hours, and then the Fed took over. U.S. retail sales for May rose 0.9%, the labour market remained stable with 172,000 payrolls added and unemployment at 4.3%, and inflation stayed too hot for comfort, with May CPI at 4.2% year on year and core CPI at 2.9%. That is not recessionary enough for easy cuts and not disinflationary enough for complacency.

The Fed’s response reflected that mix. The committee held rates steady at 3.50%-3.75%, but its projections and market interpretation were hawkish: policymakers leaned towards at least one hike this year, short-dated Treasury yields jumped, and the market moved to price a much higher chance of a year-end increase. Warsh’s emphasis on rethinking communication, including scepticism around the dot plot and forward guidance, only added to the sense that the easing bias is gone. The market is no longer debating when cuts arrive. It is debating how high the Fed’s tolerance for sticky inflation has become.

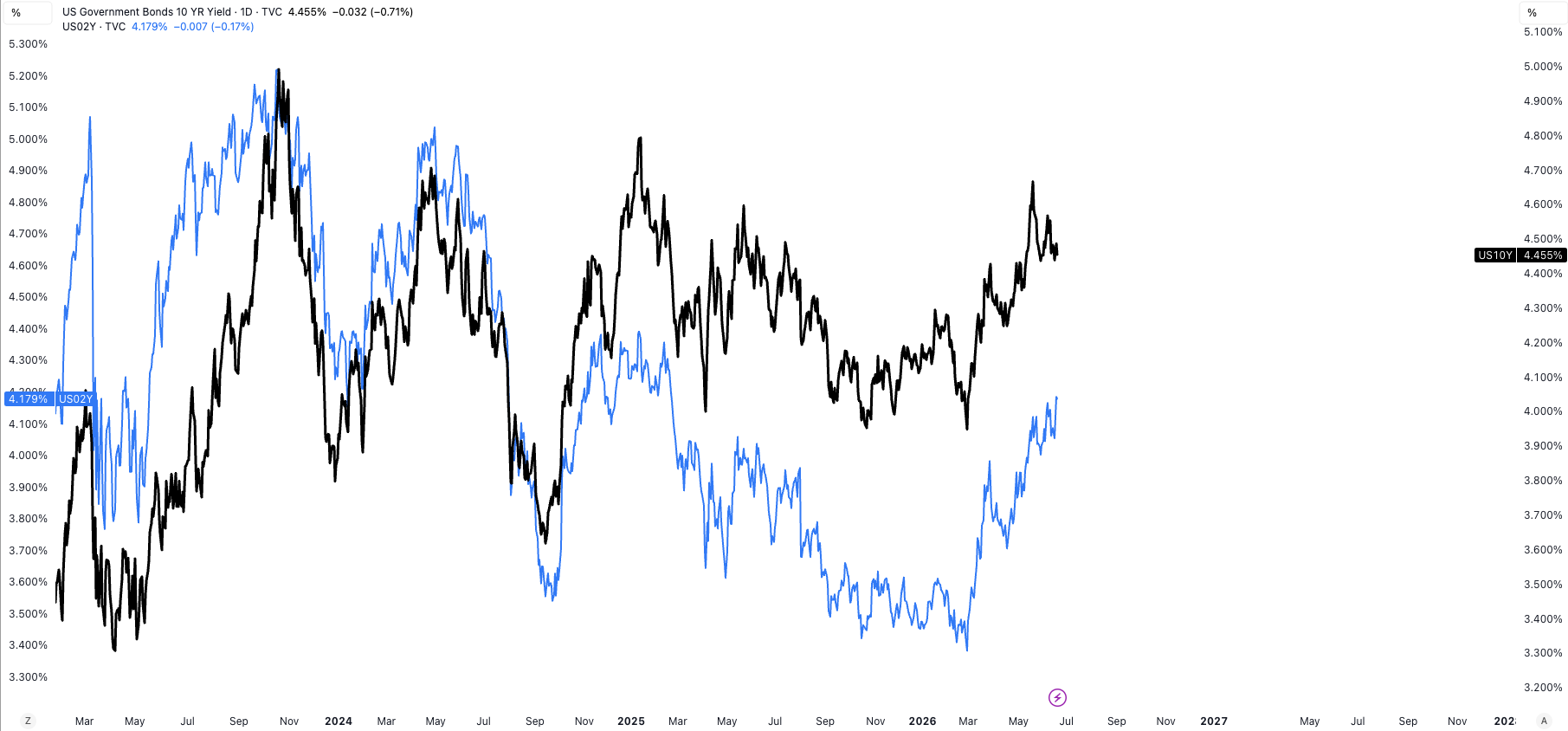

That reset matters for crypto because it changes which yield matters most. The front end still anchors policy expectations, but the long end sets mortgage rates, discount rates and refinancing conditions. There was a brief reminder of that early in the week when cooling Iran-war fears pushed the 10-year Treasury yield lower and the average 30-year mortgage rate down to 6.47%. Yet the relief was fragile. As U.S.-Iran talks frayed again into the weekend and Iran threatened renewed closure of Hormuz, oil downside lost credibility and one of the easiest channels for a disinflationary macro repricing started to close.

Our macro conclusion is unchanged in spirit but updated in emphasis. The downside is not cleared, even if we get a temporary macro repricing lower in yields. Oil can still reprice higher if diplomacy fails. The Fed has clearly shifted hawkish. And there is a new structural force now operating on the long end: AI funding demand. That is where this week’s deeper story sits.

Strategy and STRC

The cleaner single-stock story this week is STRC. Strategy’s Stretch preferred was designed to trade near par by adjusting its dividend, but the mechanism is now working against the issuer. The outstanding size is about $10.5 billion, the dividend has already been raised from 9% at launch to 11.5%, and even with that support the security has recently traded around 87-89, implying a market yield closer to 13%. Multiple reports this week argued that the formula points to another increase, at least to 11.75% and potentially towards 12% or higher if prices do not recover.

That leaves Saylor with a narrow menu. Continuing to issue STRC at a discount is unattractive. Selling common equity can still raise cash and buy more BTC, and last week’s issuance did exactly that, but it does not fix STRC directly; it mainly shifts strain onto the common by diluting holders while topping up the dividend reserve. Strategy’s recent actions, using common issuance to buy bitcoin and add cash, and increasing the reserve to $1 billion, tell you the company is prioritising liquidity and optionality, not resolving the preferred overhang.

Our view is that there are really only three credible paths from here. One is to keep lifting the dividend and hope the market eventually pays par again, which protects credibility but raises the carrying cost of the entire capital structure. The second is to buy back or tender for STRC below par, which is economically attractive if Strategy can use a still-elevated common equity multiple to fund it. The third is to keep selling common stock while the mNAV premium exists, building cash until the company can more aggressively defend or retire the preferred. Of those, the buyback/tender route looks the cleanest economically, the dividend hike route looks the most credible optically, and pure common dilution looks like the default bridge, not the endgame.

That last point is the important one: diluting common to buy more BTC may support the bitcoin narrative, but it does not solve the STRC problem on its own. That is an inference from the structure rather than a stated company plan.

Bottom line

The weekly message is simple. Last week’s “technical reversal, not final low” still stands. Crypto stabilised, but it did not break free. Macro got a brief oil-led reprieve, but the Fed replaced it with a hawkish repricing. The deeper medium-term issue is that AI capex is no longer just an equity valuation story; it is becoming a capital-markets story that can keep the long end firmer than bulls want.

So the right posture remains the same as last week, just with a sharper macro lens. Respect the bounce. Be open to relative crypto-versus-tech opportunities if that ratio keeps leaning on long-term support. But do not confuse a tactical reversal with cleared downside. We still do not think the downside is cleanly behind us, even if yields retrace a bit and oil stays softer for a few sessions. For that call to improve materially, we would want a calmer long end, less hawkish Fed pricing, cleaner ETF participation, and evidence that the STRC problem is being solved rather than financed around.