It was a challenging week for crypto markets, with Bitcoin breaking below the psychological $80,000 mark for the first time in nine months. BTC plunged to an intraday low around $76,000 before finding support and stabilising in the high-$70ks.

This sell-off has left technical indicators flashing oversold – Bitcoin’s daily RSI and Stochastic oscillators dipped well into oversold territory, suggesting the downtrend may have been overdone in the short term. For now, $80,000 (the former floor) has become immediate overhead resistance, while the $77,000 zone, roughly corresponding to Bitcoin’s cost basis for large holders, is the new line in the sand that bulls are defending. A clear break of 77k, opens up for 74k/67/65k.

Broader market capitalisation is also teetering on a crucial threshold. The total crypto market cap has slipped below $3 trillion and is fast approaching a structural support trendline that has underpinned the market since 2024.

The 2.45T is key support, and would open up for further correction towards $2T mark.

Macro

Markets were rocked by a cocktail of geopolitical and monetary shocks. Over the weekend, rumors of a potential U.S. strike on Iran circulated across media outlets.

While the strike was never confirmed, the mere hint of escalating conflict in the Middle East sent crypto lower. The last time this occurred – during mid-2025 – a brief but violent risk-off episode followed, market were quick to reprice geopolitical risk into portfolios.

Adding to this volatility, President Trump’s nomination of former Fed governor Kevin Warsh as the next Fed Chair sent markets into a tailspin. Warsh is widely viewed as an inflation hawk with a history of skepticism toward QE and ultra-accommodative policy. Equities fell, the dollar surged, and gold and silver posted their largest one-day drop in decades. The market interpreted the nomination as a potential return to stricter monetary discipline – especially unwelcome in a week already marked by rising tensions and fragile liquidity.

That said, views on Warsh are evolving. Some analysts believe his prior hawkish stance may soften under political pressure and a shifting macro landscape. In 2025, Warsh aligned with the Trump administration’s push for lower rates. This dichotomy – between his legacy image and recent behavior – has created uncertainty about what kind of Fed he will lead. The consensus is that he may turn more pragmatic in the near term, even if structurally conservative in the long run. The initial market reaction may moderate if Warsh telegraphs dovish flexibility.

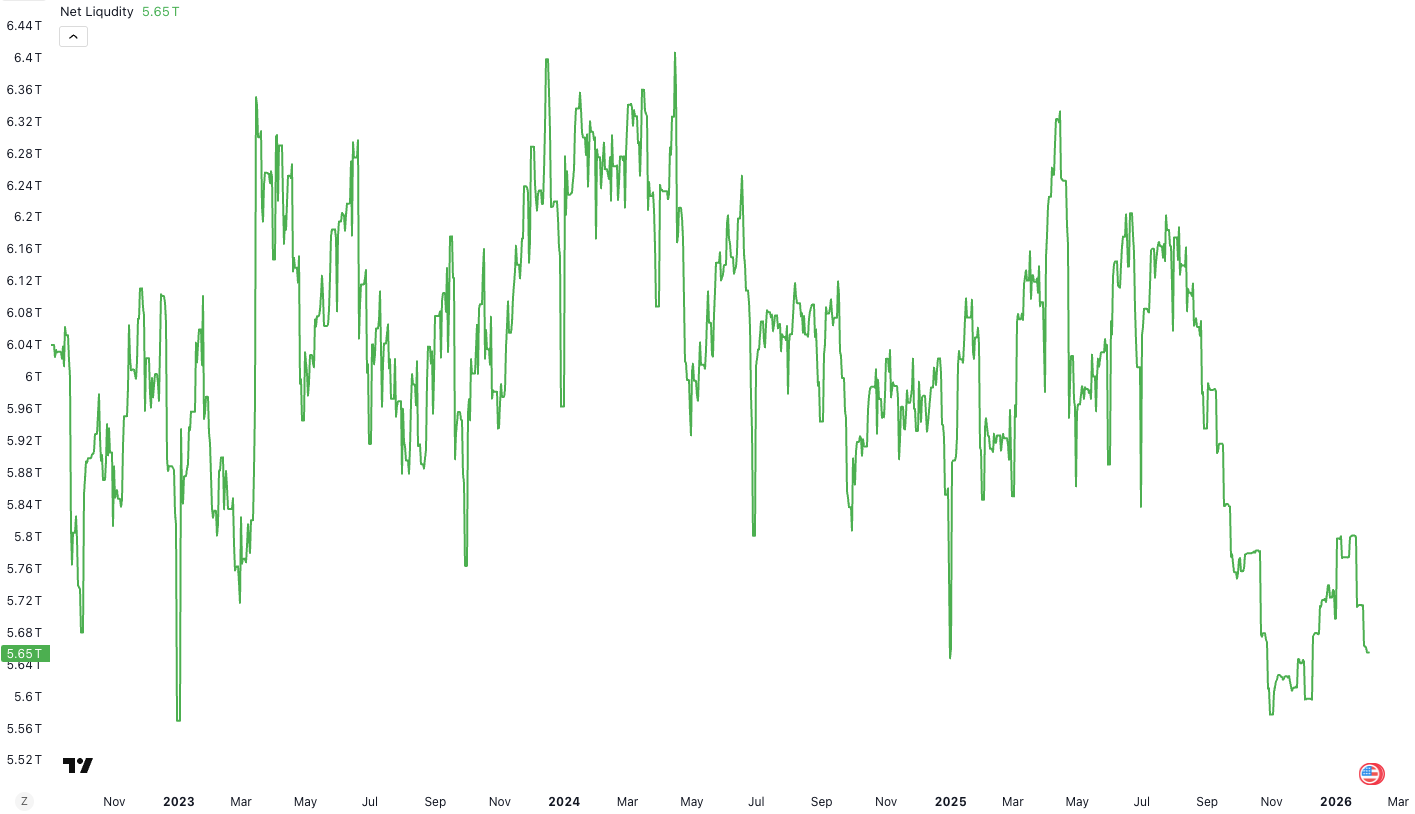

Meanwhile, net liquidity in the U.S. financial system continues to deteriorate. The Fed’s balance sheet runoff combined with increased Treasury cash balances reduced net liquidity from $5.8T (mid Jan) to $5.66T over the past two weeks. This contraction, driven by Treasury’s TGA rebuild, most likely ahead of government shutdown, is particularly negative for high-beta assets like crypto. Reduced liquidity removes a crucial tailwind that had supported price stability throughout 2026.

Institutional Rotation and Equity Crosswinds

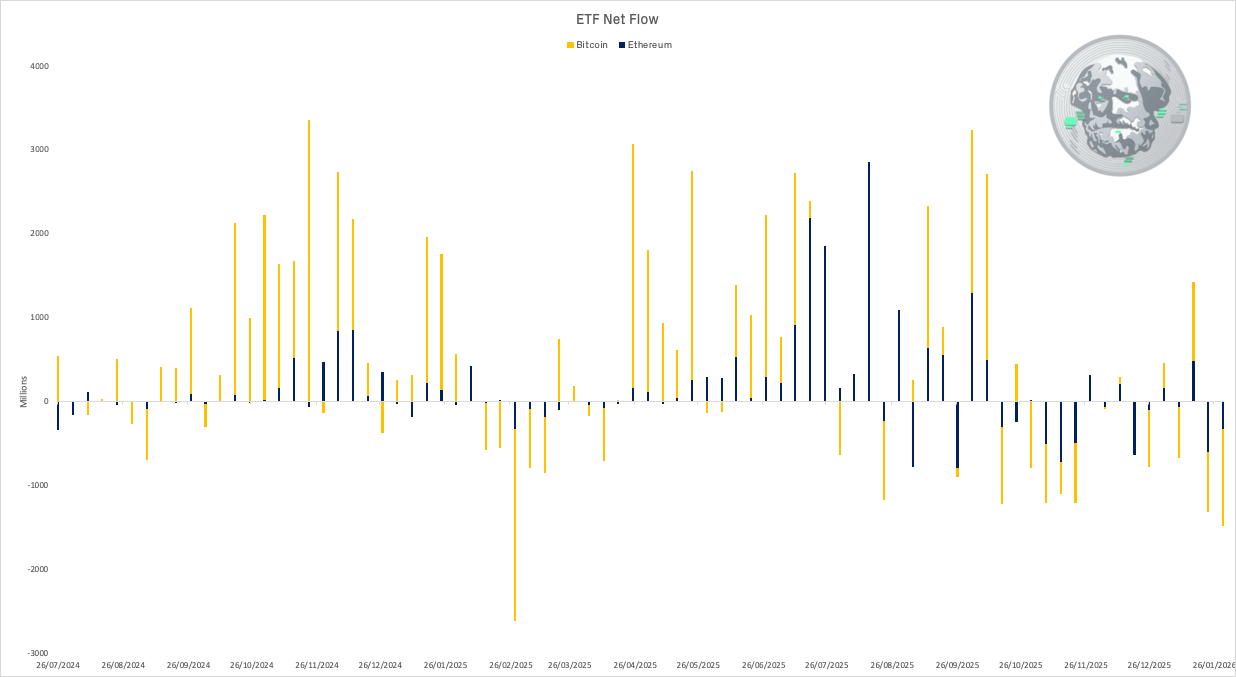

Flows into institutional crypto products turned deeply negative. Bitcoin-focused ETFs saw $818 million in net outflows on Jan 29 alone – the largest single-day redemption on record. Ethereum ETFs followed suit, with $327 million in redemptions that same week.

This kind of exodus shows hedge funds and asset managers de-risking their exposure in response to Fed policy uncertainty and macro volatility.

Crypto-exposed equities weren’t spared. MicroStrategy, now rebranded as “Strategy,” saw its BTC position briefly turn red as BTC dipped below the firm’s ~$76,000 cost basis. Saylor reiterated there would be no forced selling, but MSTR shares still lagged.

Meanwhile, BitMine Immersion (BMNR), an ETH treasury play, was hit even harder. Holding over 4.2M ETH at an average cost above $2,500, the firm is sitting on an unrealized $6B loss. Their aggressive accumulation strategy is now under scrutiny, even though insiders say the firm remains committed.

Elsewhere in big tech, Microsoft posted strong earnings led by AI services. OpenAI-driven cloud usage boosted Azure revenue 39% YoY, but higher-than-expected capex spooked some investors, and the stock fell. That pressure spilled into Nasdaq and indirectly into crypto, which has increasingly traded as a macro-proxy for growth and innovation bets.

Global Watch: Japan’s Election and Risk Contagion

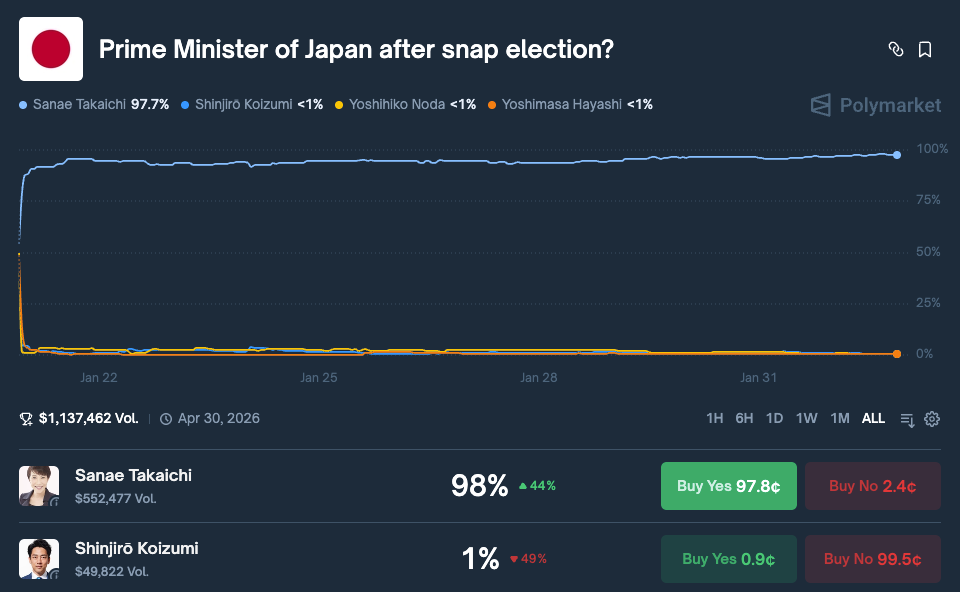

Japan’s snap election (Feb 8) is shaping up to be a major macro event. PM Sanae Takaichi is expected to win a stronger mandate, which would embolden her fiscal expansion plans.

Markets reacted by pushing Japanese yields to 25-year highs and whipsawing the yen. A bigger LDP majority could further steepen JGB curves and increase inflation risks.

Global bond markets are watching closely: rising Japanese yields may force Japanese capital back home, impacting U.S. Treasury demand and global rates. For now, volatility in Japanese assets is bleeding into FX and equities, adding another layer of risk to global positioning.

Sentiment & Outlook

Heading into the week of Feb 3, markets remain on edge. Equities are soft, crypto is oversold, and metals just experienced one of their worst sessions on record. Volatility is elevated, but not unmanageable. This suggests a sentiment reset may already be underway. Still, the macro picture remains messy: liquidity is tightening, central bank uncertainty is high, and geopolitical risk remains unresolved.

A tactical bounce is possible given the extent of the washout. But sustainable upside will likely require one of three things:

1) A dovish pivot from the Fed or incoming Chair,

2) Calming geopolitical news, or

3) A shift in liquidity policy (e.g. TGA Drawdown), depending on the US shutdown.

Until then, expect high volatility trading with intraday spikes and liquidations on both sides. The market remains fragile, but also full of opportunity for those with discipline and patience. This is not yet the beginning of a new bull leg, but it may be the middle of a correction that’s doing its job: flushing leverage, resetting sentiment, and clearing the way for healthier price discovery ahead.

Medium-Term Outlook: We see elevated risk for further downside in the weeks ahead. While crypto has corrected sharply, U.S. equities have yet to meaningfully pull back. If equity markets begin to reprice stretched valuations, particularly in growth sectors sensitive to rising rates and capex pressure (AI, cloud, tech) – it will likely drag risk assets lower across the board. With Japan's election adding to global bond volatility and the Fed’s direction still uncertain, crypto may not be out of the woods yet.

Really solid synthesis of the week's macro cross-currents. The Japan election angle is underapreciated imo because if Takaichi gets her mandate and JGB curves steepen materially, the captal repatriation flow could hit US equities harder than most expect. I saw similar dynamics play out in 2023 when Japanese institutions started unwinding overseas positions. The crypto sell-off feels overdone technically but macro setup is still kinda messy with liquidity tightning.