The core story remains the same: crypto is trading inside a regime defined by geopolitics → energy → inflation expectations → rates. This week delivered a sharp example of that chain: a ceasefire headline briefly eased the “war premium”, then the latest round of talks broke down and the market reverted towards tension risk centred on the Strait of Hormuz.

Bitcoin continued to trade within the well-defined $65k–$75k corridor we highlighted previously, with upside attempts fading near the top of the range and downside protection still holding above the mid/high‑$60s.

On the macro side, March CPI was dominated by the energy shock: headline inflation printed hot, but the core leafed in softer than consensus, leaving the Federal Reserve with the same uncomfortable mix of inflation pressure and slower/uneven labour signals.

Separately, the “AI capex” risk cluster we’ve flagged before tightened: Bloomberg reported that a large share of planned US data centres are being delayed or cancelled, and OpenAI paused a major UK data-centre initiative, explicitly pointing to regulation and energy costs, both of which also connect back to the energy shock.

Crypto

BTC spent the week oscillating inside ~$67.7k–$73.8k, consistent with the broader 65–75k corridor. The week’s low printed on 7 April as the “deadline/ultimatum” rhetoric dominated, while the local high printed on 11 April as markets leaned (briefly) into the weekend diplomacy window.

From a structure perspective, the key point is unchanged: a re‑escalation of the conflict that drags oil risk premia higher again is still the cleanest path to re-testing the lower band of the range; a credible de‑escalation and normalisation of traffic through Hormuz is still the cleanest path towards a sustained push above ~$75k. The “range until proven otherwise” framing is also consistent with our 23 March note.

ETH tracked BTC’s tape but with a clearer “hold the level” narrative: it briefly traded up to printed on 7 April. Importantly, ETH spent much of the week fighting to remain around ~$2.2k, with a softer close into Sunday.

Geopolitics and the energy channel

The centre of gravity stayed with United States–Iran dynamics, and specifically the “control of Hormuz” dimension. The most consequential development for the weekly tape was that high-level talks in Islamabad, Pakistan ended without an agreement after marathon negotiations led on the US side by JD Vance. with uranium enrichment and Hormuz control among the core sticking points.

Early in the week, oil prices were still reflecting “escalation risk” around the deadline posture. Then, ceasefire headlines triggered an air‑pocket move lower: reporting described Brent falling ~15% on 8 April , one of the sharpest daily drops since 2020.

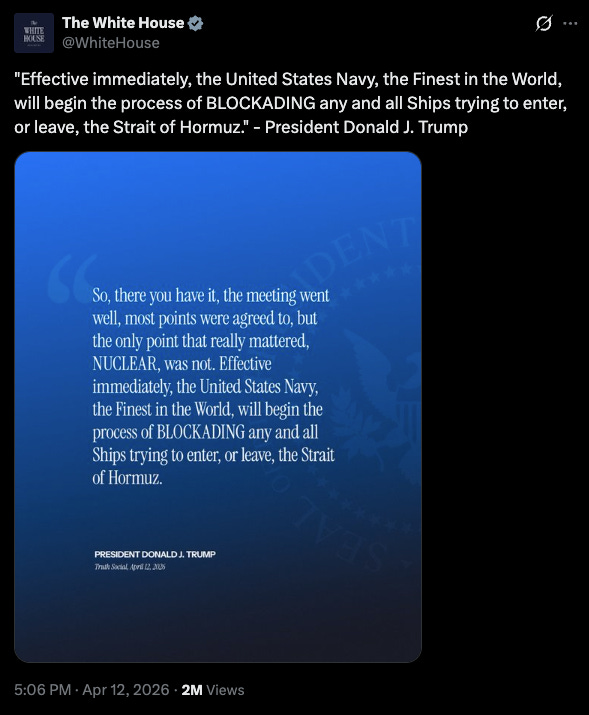

But the week ended with renewed stress as talks collapsed: Donald Trump publicly threatened a US Navy blockade in response to the lack of agreement, and markets immediately re-focused on what “freedom of navigation” looks like in practice over the coming days.

Even during the “ceasefire optimism” window, shippers emphasised they needed clarity on terms before resuming normal transit, and Reuters reported substantial trapped inventory and ongoing maritime risk.

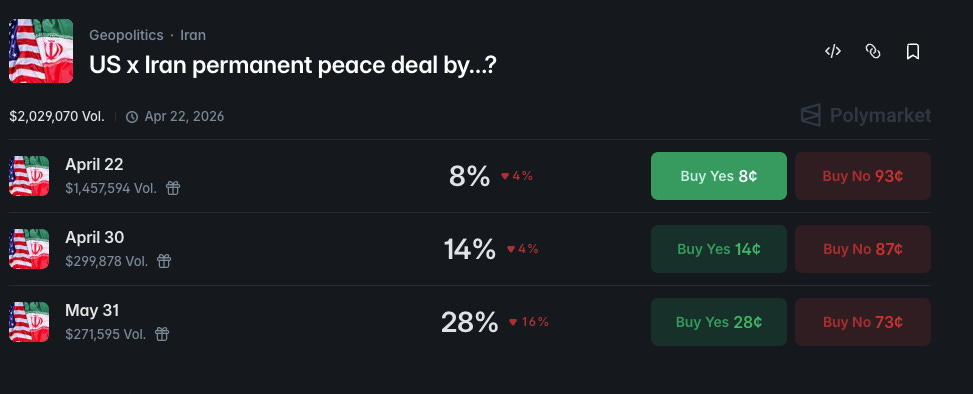

On Polymarket, the “US x Iran permanent peace deal by…?” market implied low odds of a near-term permanent deal as of

22 April, 8%

30 April, 14%

31 May, 28%

Macro and rates

The week’s macro picture can be summarised as: headline inflation is being pushed around by energy, while the core trend is less explosive, but still sticky enough to keep the Fed cautious.

In the March CPI release, the energy index rose 10.9% in March, and gasoline rose 21.2% (BLS notes this was the largest monthly increase in that series since it began in 1967). This is an inflation shock tied to the Iran war’s impact on energy prices, with CPI up 0.9% m/m and 3.3% y/y, while core inflation was more moderate at 2.6% y/y.

Weekly jobless claims rose to 219,000 for the week ending 4 April (up from 203,000 prior), exceeding consensus and marking the highest level since early February, while continuing claims fell.

This keeps the Fed in the “tricky seat” described in the draft: growth signals are not collapsing, but inflation sensitivity has increased, and labour is no longer a one-way “too tight” story.

At the March meeting, the Fed held the target range at 3.50%–3.75% and explicitly noted that Middle East developments add uncertainty to the outlook.

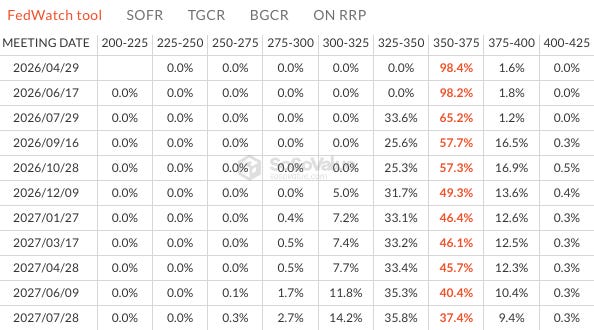

This week, the market’s rate-cut narrative shifted with the ceasefire headline: CME FedWatch-implied odds of a rate cut by end‑2026 jumping sharply after the ceasefire announcement.

But the “no permanent resolution” outcome re-raises the risk that energy stays higher for longer, and that the Fed chooses caution over easing. The post-ceasefire shift improved rate-cut odds but still leaving a cut “unlikely,” expectations of hold.

Risk assets, AI , and Software

Two cross-asset observations mattered this week: (1) energy is rewriting the macro constraint set; (2) the AI trade is becoming more internally inconsistent, with infrastructure bottlenecks meeting valuation sensitivity.

Equities wobble, software breaks, crypto holds up better.

It was a tough week for software: the iShares Expanded Tech-Software Sector ETF (IGV) saw a sharp drawdown, while BTC moved the other way, staging a rebound. That divergence challenges the idea of crypto, particularly BTC, as a clean “risk-on proxy” for this corner of equities, and raises the possibility that the long-standing correlation is starting to break.

The split is clear in the weekly numbers: IGV dropped roughly ~7% between April 6–10, while BTC posted gains over the same Mon–Fri window, and even after Sunday’s fade, still closed above the prior week’s levels.

AI: The “plumbing” is the constraint.

Bloomberg reported that a large share of US data centres planned for 2026 are expected to be delayed or cancelled, citing shortages in electrical equipment (transformers/switchgear) as a key bottleneck. TechRadar’s write-up of the same Bloomberg reporting framed the scale as “nearly half,” linking delays to supply-chain constraints, power availability, and local opposition, exactly the kind of real-economy friction that can puncture AI narratives even when capital is available.

Reuters reported that OpenAI paused a major UK data-centre project, explicitly citing regulation and high energy costs, reinforcing the idea that “energy prices and permitting” are now first-order variables for AI infrastructure rollouts.

Our take remains consistent with the draft: if geopolitics calms and oil risk premia compress, risk can rally and crypto with it. But the AI build‑out increasingly looks like it can be slowed by non-chip constraints, leaving the second order effects of chip making aside, and that keeps the “AI bubble / AI capex disappointment” risk live, especially if equities continue to de-rate.

Policy and regulation

The regulatory narrative is “incremental progress, but not an immediate tape driver.”

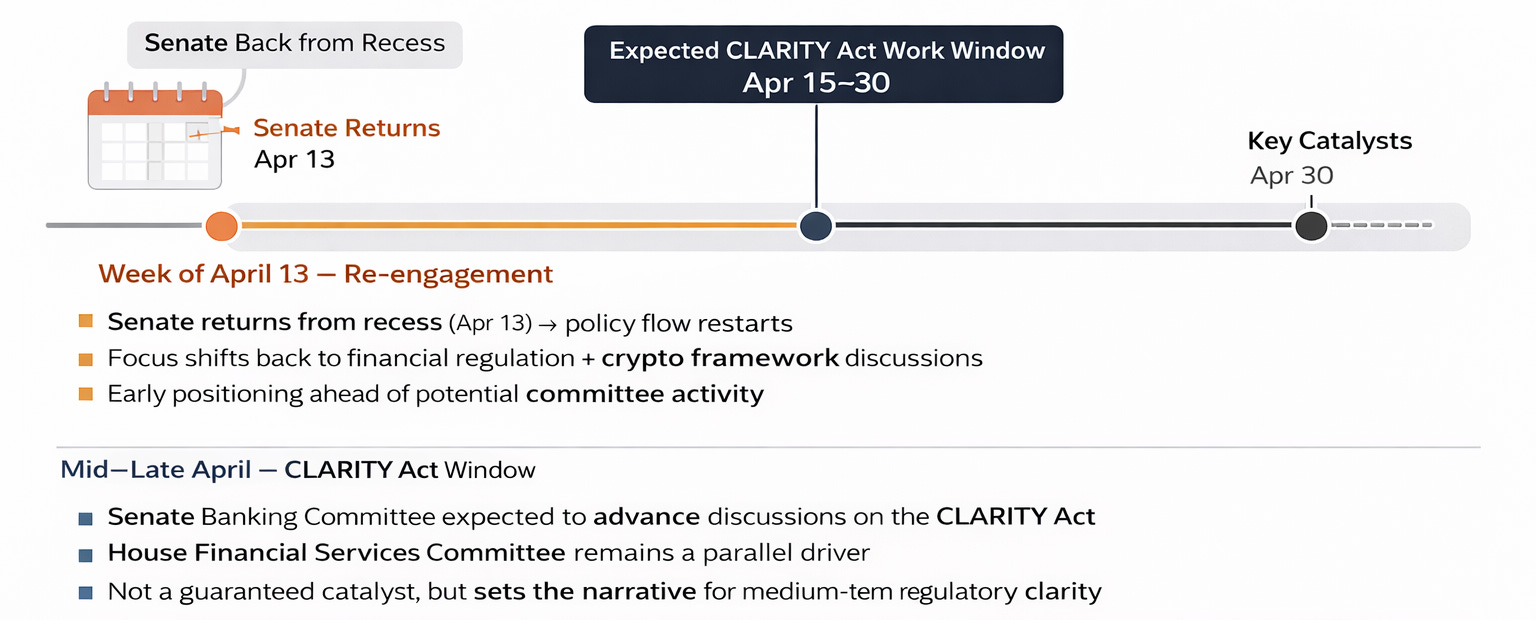

CLARITY Act: pressure is rising, calendar is still the calendar.

Reuters reported that Scott Bessent urged Congress to pass the CLARITY Act, arguing the US needs a clearer federal framework for digital assets.

On timing, crypto press reporting indicated Bill Hagerty said at an event at Vanderbilt University that Republicans planned to begin moving the bill through the Senate Banking Committee “starting next week.”

However, as of 12 April, the official markup calendar page for the Senate Banking Committee shows the last listed item in 2026 as a postponed January executive session, with no April markup date posted there yet.

This keeps the base case intact: policy progress is a medium-term unlock, but it is unlikely to overpower a geopolitically-driven downtrend by itself if the energy shock remains the dominant macro input.

Looking ahead

The coming week is still about sequencing, not narratives.

First, the geopolitics–oil linkage remains the gatekeeper. Even during ceasefire windows, shipping and transit normalisation has been conditional and fragile; if markets sense “traffic normalisation is failing,” oil risk premia can reassert quickly.

Second, in the 23 March Insider we framed the environment as a four-phase playbook

Denial → Realisation → Liquidation/opportunity → Rebuild.

In our read, this week looked like a brief Denial-adjacent bounce (ceasefire optimism) that quickly reverted towards Realisation once the diplomacy failed and inflation data kept the “rates constraint” in view.

Third, watch whether BTC continues to hold up relative to software and broader risk proxies. The recent divergence matters, if sustained, it would be one of the few genuinely “new” signals in an otherwise unchanged regime, hinting that crypto may be starting to decouple at the margin.

From a levels perspective, the range remains clearly defined:

$65k → key support. A loss here likely signals escalation (macro/geopolitical), opening downside into the low $60s.

72k → mid-range / local pivot. Acceptance above keeps short-term momentum constructive.

$75k → range high. A clean break likely requires de-escalation and/or a tailwind from macro (oil lower, rates repricing).

Until one of these breaks decisively, BTC remains range-bound, with positioning dictated more by external catalysts than internal momentum. The rest of the market is likely to continue taking cues from BTC, trading in a high-beta fashion to its moves.

We remain cautious in the short term.