The final week of August closed with divergence across majors and a marked shift in capital flows. Bitcoin retreated into seasonal weakness, Ethereum extended its outperformance versus BTC, and altcoins began to build relative momentum.

Beneath the surface, a single whale rotation is materially influencing ETHBTC and forcing traders to reassess positioning.

At the same time, the macro backdrop enters a critical phase. The next two weeks bring the key labor and inflation data that will either validate or undermine the market’s conviction in a September Fed rate cut. Risk assets, including crypto, are priced for easing, confirmation opens the door to acceleration, while disappointment likely drives repricing lower before Q4.

BTC: Seasonal Drag and Whale Supply

Bitcoin ended August down -2.95%, consolidating around $109K after rejection from resistance at 117K.

Currently sitting on the main resistance/support level. Liquidity clusters are well defined. The first major band of support sits between 95K and 100K, where prior demand has consistently absorbed selling pressure. Should weakness extend further, the next deeper area of structural support is found near 85K, a zone that also coincides with broader macro liquidity levels.

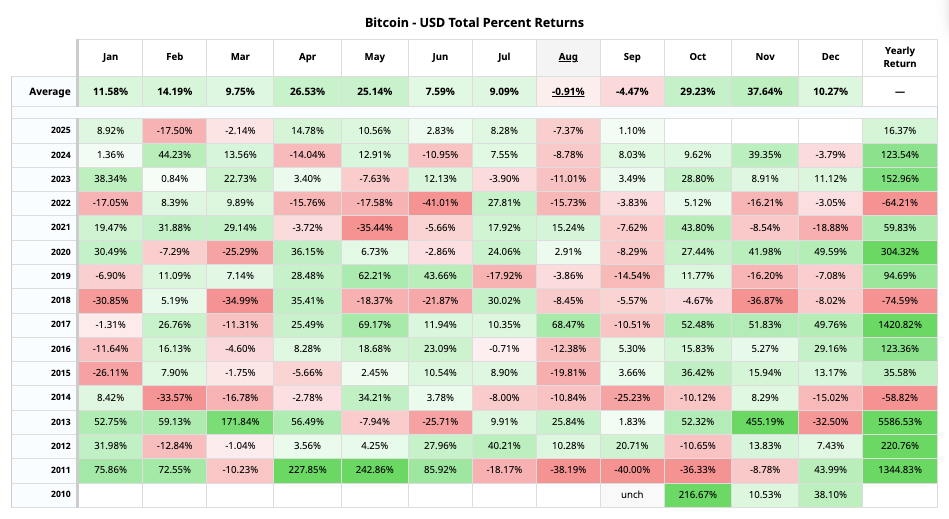

From a structural perspective, Bitcoin is entering September under clear seasonal and technical pressure. Historically, September has been the weakest month for BTC performance, with average returns of –4.5% over the past decade. This seasonal headwind is now aligning with deteriorating momentum. The daily RSI has rolled over into the high 30s, signalling that trend strength has faded and that downside follow-through remains likely.

At the same time, Bitcoin dominance has fallen to 58%, marking a decisive shift in relative strength away from BTC and into ETH and large-cap altcoins. T

This decline in dominance reinforces the broader narrative: Bitcoin is no longer the sole driver of flows in this market. Instead, it is increasingly functioning as the funding source for rotation into assets with stronger relative momentum.

Adding to structural weakness is direct supply pressure. An address tied to historic HTX withdrawals has reawakened, unloading 32,000 BTC over two weeks.

The investor still holds over 50,000 BTC, one to watch closely.

While BTC remains the cycle anchor, it is increasingly becoming the funding leg of rotation rather than the primary beneficiary of flows.

ETH: Structural Outperformance, Whale-Driven Rotation

Ethereum continues to build structural momentum and has become the clear leader in relative performance. August marked one of the strongest monthly moves in years, with ETH/BTC rising by more than 33%, a shift that has fundamentally altered the market’s perception of leadership.

Unlike earlier phases of rotation, where ETH’s strength was attributed to ETF flows or cyclical interest in DeFi, the current outperformance has been driven by concentrated flows from digital asset companies + whale rotation.

Over the past two weeks, a single entity has sold more than 30,000 BTC (~$3.3 billion) while accumulating nearly 870,000 ETH (~$3.8 billion). The activity has been deliberate and systematic, primarily routed through Hyperliquid, and remains ongoing. With over 52,000 BTC (~$5.7 billion) still under control, this whale continues to transfer coins with the intention of converting further into ETH.

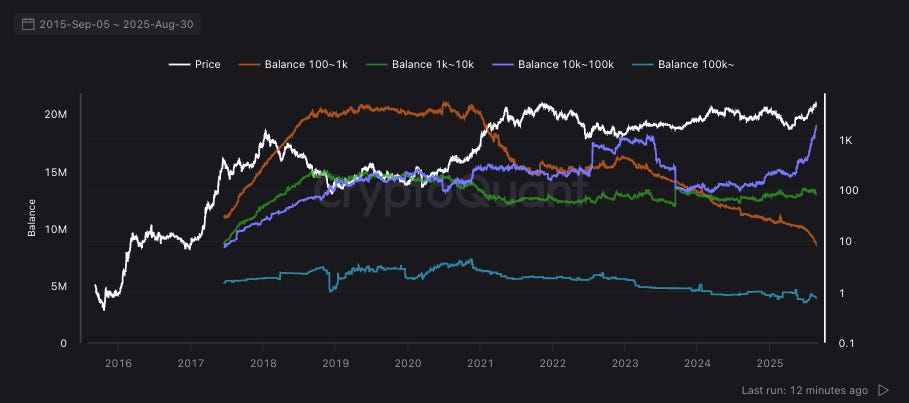

The impact of these flows extends beyond short-term relative price action. On-chain distribution data shows a structural reshaping of the Ethereum holder base. Whales in the 10k–100k ETH cohort have been net accumulators, steadily adding to their balances even as smaller holders in the 100–1k ETH cohort have reduced exposure. This divergence signals consolidation of supply into stronger hands at the same time that a single whale rotation is providing a persistent structural bid.

Taken together, this paints a picture of Ethereum entering a potential leadership phase. The combination of whale accumulation, redistribution from weaker to stronger hands, and a historically significant BTC → ETH reallocation sets the stage for ETHBTC to extend beyond a tactical trade and into a multi-month structural trend. If the remaining BTC held by the rotation whale is converted, the scale of demand could rival earlier inflection points such as the 2017 breakout and the 2020–2021 DeFi-led expansion, both of which marked prolonged periods of ETH-led market leadership.

Altcoins: Rotation Broadens Beyond Majors

Outside of ETH, the broader altcoin complex has begun to show evidence of constructive rotation. The OTHERS index (ex top 10) ended August up nearly 7%, while the total market capitalisation registered a modest but positive +0.7% gain.

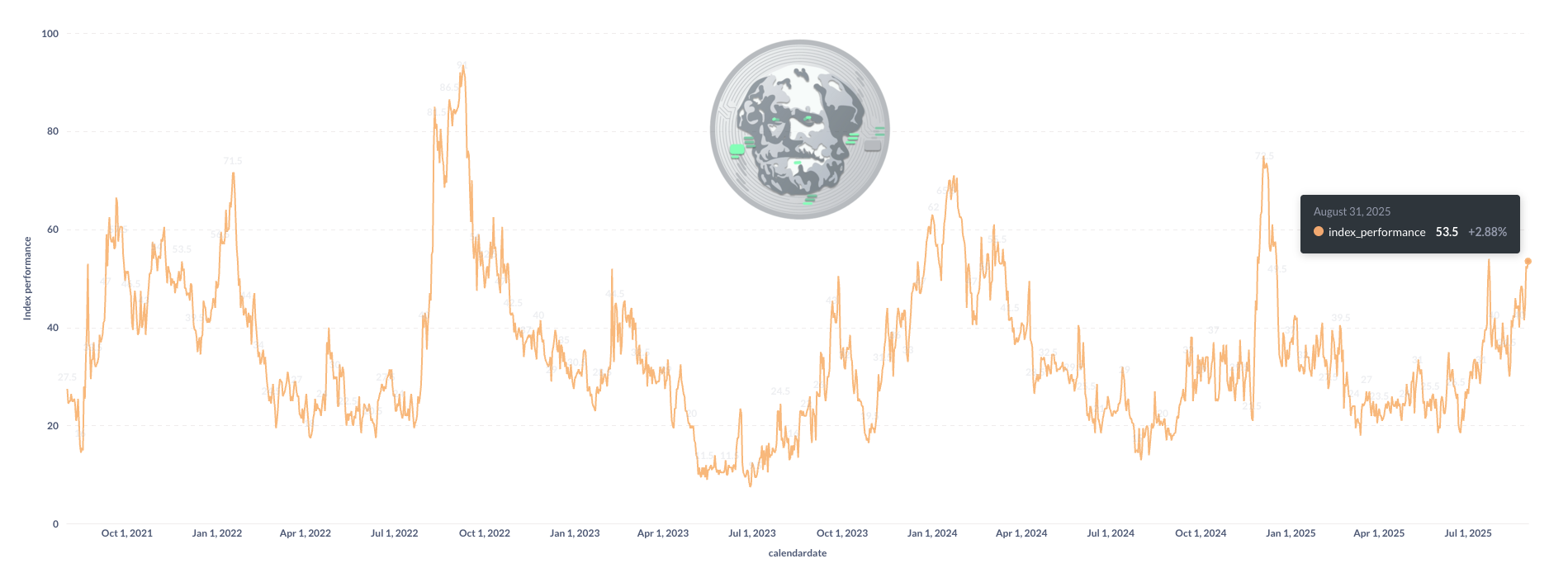

These numbers may appear muted in isolation, but under the surface the distribution of outperformance is instructive. By looking at the top 200 assets performance vs BTC with a 90D lookout period, 53.5% have outperformed BTC.

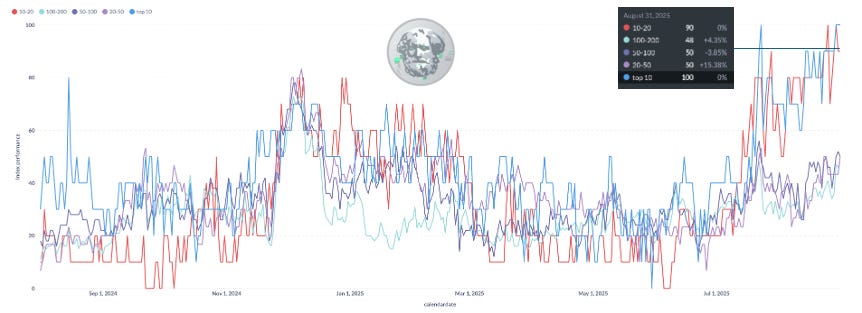

The large-cap segment is currently leading the way. Within the top 10 assets, every major has outperformed Bitcoin on a 90-day basis, while the 10–20 ranked cohort is showing nearly the same breadth, with 90% outperforming BTC.

Mid-cap names are less consistent but remain positioned for catch-up. Roughly 50% of the 20–50 group, 50–100 group, 100–200 group have outperformed BTC over the past three months.

This is a familiar sequencing pattern. Historically, rotation first concentrates in BTC, then shifts into ETH, before spreading into the top 10 and large-cap sector leaders. Only after liquidity is established in these names does the cycle typically extend into mid-caps and eventually the long tail of smaller tokens. The current setup suggests we are still in the early to middle stage of this process.

Structural charts of total market cap excluding BTC and ETH reinforce this view, with the index pressing up against multi-year resistance. A confirmed breakout would mark the formal transition from consolidation into acceleration, contingent on macro conditions aligning with the rotation already underway.

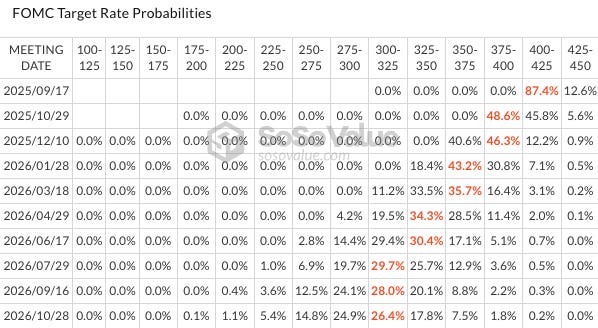

Macro: A Binary Data Window

The macro backdrop has entered its most consequential stretch of the quarter. Risk markets, including crypto, are trading with an implicit assumption that the Federal Reserve will deliver its first rate cut in September.

Fed funds futures currently price an 87% probability of a 25bps reduction, making easing the consensus position. That consensus will now be tested by a sequence of data releases over the next two weeks.

The first test arrives this Friday with US Non-Farm Payrolls (NFP). Labor softness is a necessary condition for validating near-term easing, as the Fed has repeatedly tied policy flexibility to signs of cooling employment.

Next week’s CPI release on September 11th is equally pivotal. Continued disinflation, particularly in core services, is required to offset stickier inflation expectations. The final arbiter will be the FOMC meeting on September 17th, where the Fed will either confirm market pricing or force a repricing across rates, FX, equities, and crypto.

The setup is binary. If the data confirm, the market is positioned for broad risk acceleration, with ETH and large-cap alts standing to benefit most from liquidity expansion. If the data disappoint, risk assets face a sharp repricing lower as traders unwind the aggressive front-loading of easing expectations. Elevated volatility across bonds and FX suggests positioning is fragile, and crypto’s alignment with the “cut confirmed” scenario amplifies asymmetry.

For Bitcoin specifically, this timing is challenging: September is historically its weakest month, and whale-driven supply adds further pressure. Ethereum and large caps, by contrast, are positioned as the highest beta beneficiaries of easing. In short, the macro path over the next two weeks will determine whether the current ETH-led rotation extends into Q4 or stalls under the weight of tighter policy expectations.

Market implications

The market is entering a decisive moment where internal rotation and external policy converge. On one side, whales are reshaping the ETHBTC curve and accelerating the shift in leadership away from Bitcoin. On the other, macro conditions will determine whether this transition is validated by broader liquidity or stalled by tighter policy.

The next two weeks will not just set the direction for September, they will define whether the current rotation becomes a sustained regime change or a temporary dislocation. In that sense, crypto is no longer waiting for inflows; it is already being repriced from within.

One whale is reshaping ETHBTC; one Fed meeting will decide whether that rotation accelerates into Q4 or stalls.