Bitcoin entered the week already vulnerable. Price had failed to reclaim the $80k resistance zone, and momentum was rolling over as equities softened. Once $77k gave way early in the week, selling accelerated rapidly. Liquidity thinned, stop levels were triggered, and forced liquidations dominated flows.

BTC ultimately printed a low near $60,000, marking a 24% drawdown from the highs in a matter of days. The speed of the move is what mattered most. This was not orderly distribution but mechanical deleveraging, driven by futures liquidations, risk parity adjustments, and broader macro selling.

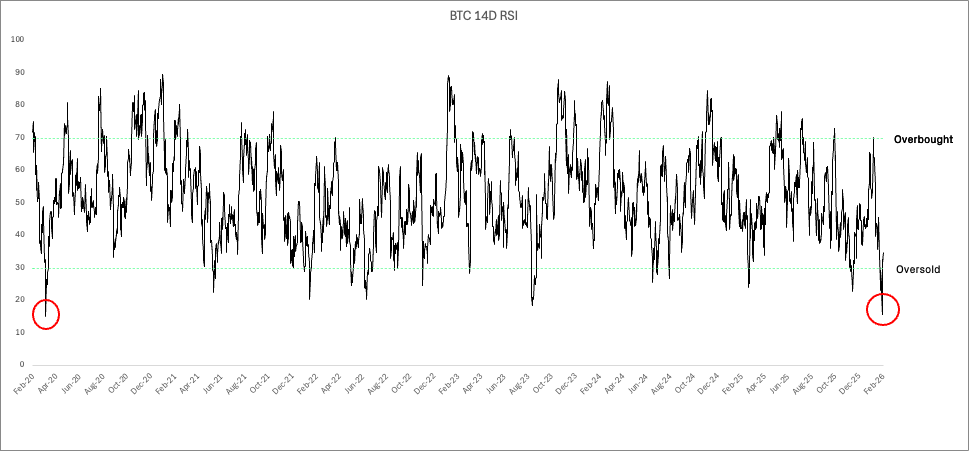

The most notable technical signal was momentum exhaustion. Bitcoin’s daily RSI collapsed to approximately 16.6, a level last observed during the March 2020 COVID panic. Historically, RSI readings below 20 have only occurred during periods of systemic stress rather than at cyclical tops. These moments tend to coincide with leverage capitulation rather than long-term trend exhaustion.

The subsequent rebound was consistent with this interpretation. BTC recovered sharply into the $70–72k area as forced sellers were cleared and short-term positioning reset. That said, structure has not yet been repaired. The $85–90k region is now clearly overhead resistance, while the $75–78k area represents the minimum reclaim required to stabilise price action. On the downside, the $60–62k zone has become critical support. A sustained failure there would materially increase downside risk.

For now, the bounce should be viewed as reflexive rather than confirmatory.

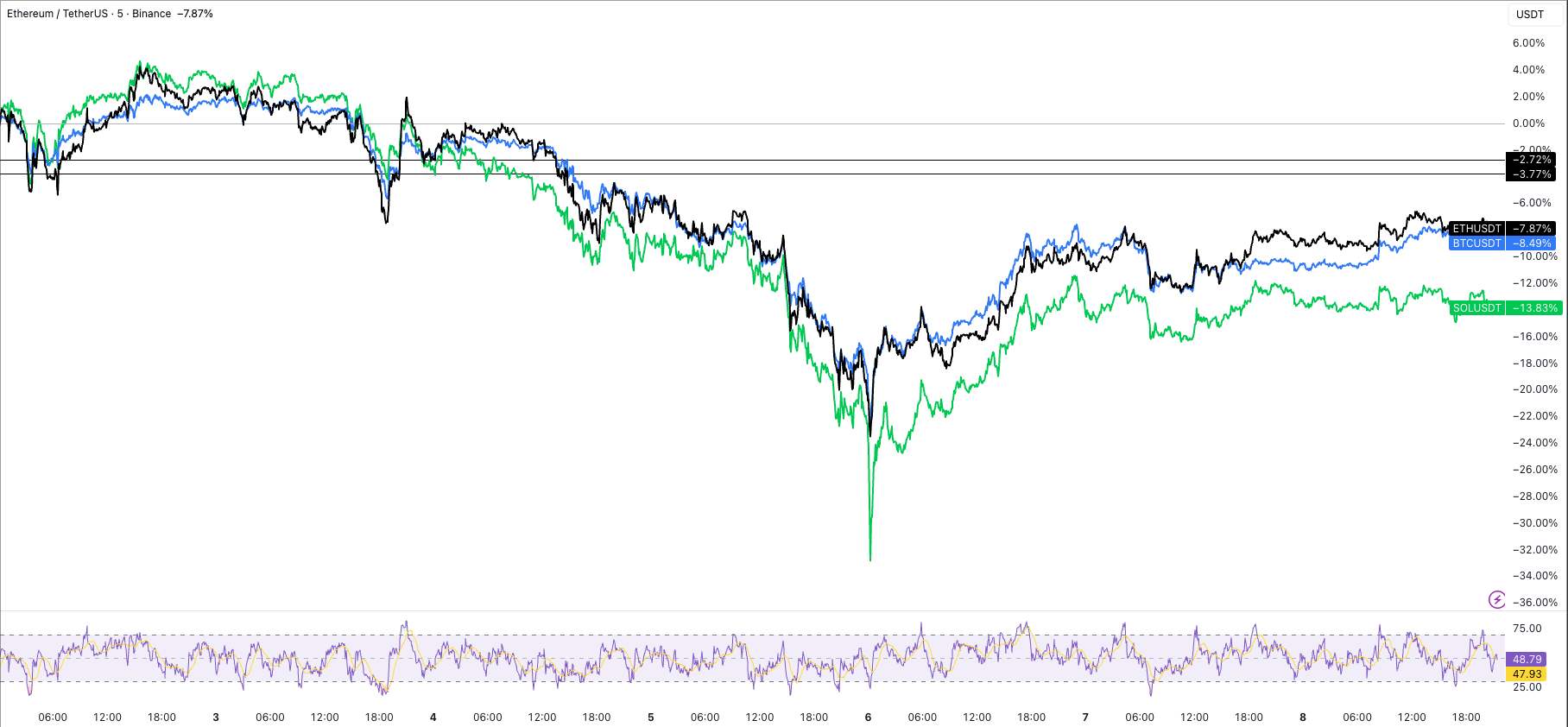

Ethereum underperformed Bitcoin throughout the move, both on the downside and during the rebound. ETH fell roughly 26% peak to trough, slicing through the $2,200 and $2,000 levels before briefly trading below $1,800.

While ETH also reached oversold momentum conditions, the structural damage is more pronounced. Prior range support in the $2,200–2,300 region has now flipped into resistance, and ETH remains well below its former value area. Relative weakness versus Bitcoin persists, reflecting ETH’s higher sensitivity to liquidity conditions and equity risk.

Total Market Cap

The clearest structural signal this week came from the total crypto market capitalisation. The $2.45 trillion level, which had acted as medium-term support throughout late 2025, failed decisively early in the week. Once lost, selling cascaded rapidly, dragging total market cap toward $2.0 trillion.

This was a broad-based liquidation. There was no meaningful rotation into defensives within crypto. Large caps, mid caps, and high-beta assets all sold off together, confirming that the move was driven by liquidity rather than narrative.

While total market cap recovered modestly into the weekend, it remains below prior value. From a structural standpoint, the market is still in repair mode. Reclaiming $2.45 trillion will be essential to re-establish bullish conditions.

Crypto = Software

One of the most important observations from this week is how tightly Bitcoin traded alongside software equities and the broader Nasdaq. Bitcoin’s price action mirrored the iShares Expanded Tech-Software ETF (IGV) almost tick-for-tick during the sell-off, while the Nasdaq itself fell roughly 7% on the week. This was not coincidence, and it was not noise.

Crypto did not sell off in isolation. It sold off as part of a broader repricing of long-duration growth assets.

The common denominator was software.

IGV is heavily weighted toward long-duration software and SaaS companies such as Microsoft, Salesforce, Oracle, Intuit, Adobe, and Palantir. These businesses benefited enormously from the prior regime of low rates, expanding multiples, and highly predictable cash flows. That framework is now being challenged simultaneously by higher discount rates and by AI-driven uncertainty around future margins, pricing power, and capital intensity.

As software equities rolled over, Bitcoin followed. This reinforces a point we’ve made repeatedly: Bitcoin like Tech continues to trade as a growth-sensitive, liquidity-dependent asset, rather than as a macro hedge or defensive store of value. Until that regime changes, equity market stress, particularly in technology and software, will continue to transmit directly into crypto.

The Nasdaq’s weakness this week provides important context. The move lower was driven less by macro data and more by earnings commentary and forward guidance, especially around AI-related capital expenditures. Several large technology firms signaled meaningful increases in AI spending, raising concerns that returns may lag investment. The market’s concern is not whether AI will be transformative, that is largely accepted, but whether the cost curve is becoming front-loaded while monetisation remains uncertain.

In response, markets compressed multiples across software, cloud, and AI-adjacent names. The Nasdaq absorbed that repricing first. IGV followed. Crypto followed last.

This sequence matters. Crypto did not lead this move; it reacted to it.

As long-duration assets with implied growth optionality, both software equities and crypto are highly sensitive to changes in discount rates and return expectations. When equity investors begin to question the durability of cash flows or the efficiency of capital deployment, those concerns propagate quickly across correlated assets. This week, equities were the transmission mechanism. Crypto was the amplifier.

The feedback loop does not stop at public markets.

A quieter but increasingly important development this week was the mounting stress in private credit, particularly among lenders exposed to software and SaaS businesses. During the low-rate era, private credit vehicles and Business Development Companies extended significant amounts of capital to software firms, underwriting stable cash flows, durable competitive moats, and predictable growth trajectories.

AI disruption complicates those assumptions.

As public software equities sold off, publicly traded BDCs followed, many now trading at significant discounts to net asset value. This reflects growing concern that loan defaults could rise, collateral values may decline, and liquidity mismatches could emerge if redemptions accelerate. In effect, the equity market is beginning to question the solvency assumptions embedded in private credit portfolios.

Private credit is not yet a systemic issue. However, it represents a latent fault line. Historically, stress in private credit markets tends to lag equity declines rather than lead them. When it does emerge, it can amplify liquidity tightening by forcing asset sales, restricting credit availability, and reinforcing risk-off behavior across markets.

This matters for crypto because liquidity is the connective tissue. A world in which software valuations compress, capital expenditure rises, and private credit tightens is a world with less marginal liquidity for speculative assets. In that environment, crypto behaves less like an alternative system and more like a downstream expression of financial conditions.

Taken together, the Nasdaq sell-off, the repricing of software equities, and emerging stress in private credit all point to the same conclusion: this was not a crypto-specific unwind. It was a growth-asset reset.

Until software stabilizes, crypto will struggle to decouple.

Macro

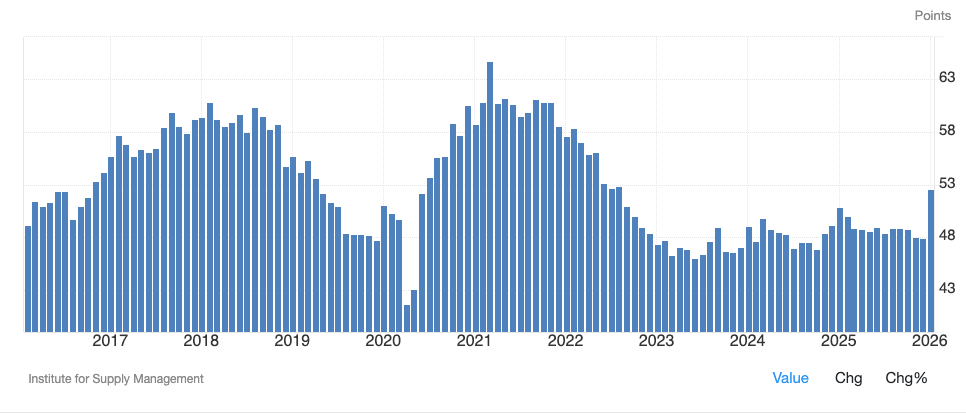

From a macro perspective, the week offered little relief. US economic data surprised to the upside, with ISM readings reinforcing the view that activity remains resilient.

While positive in isolation, this strength complicates the outlook for risk assets. Strong growth reduces the likelihood of near-term policy easing and keeps financial conditions tighter for longer, particularly at a time when valuations across equities and crypto remain sensitive to discount rates.

Layered on top of this is increasing focus on the potential policy stance of Kevin Warsh. Widely viewed as more hawkish and balance-sheet conservative, Warsh represents a Federal Reserve framework that is less tolerant of financial excess and more explicitly focused on inflation control, even at the expense of asset prices. For markets that have grown accustomed to policy backstops and liquidity support, this shift in expectations matters

For crypto, the implications are direct. The 2023–2025 rally was, at least in part, liquidity-supported. As Fed net liquidity expanded, financial conditions eased, allowing leverage to build, risk premia to compress, and valuations, particularly in higher-beta segments of crypto to expand.

That backdrop is now shifting. Fed net liquidity has rolled over, in the near term due to government shutdown, reducing tolerance for excess. In a regime defined by firmer growth, stickier inflation, and a more restrictive policy bias, markets demand lower leverage, more realistic valuation assumptions, and greater selectivity. The impact is most visible in the “OTHERS” market cap, where speculative assets are repricing first.

Japan adds another layer of complexity. It remains an underappreciated but critical macro variable in the global liquidity equation. Rising Japanese government bond yields, persistent yen volatility, and uncertainty around Bank of Japan policy introduce the risk of disruption to long-standing carry trade dynamics. Japan has historically been a major exporter of capital, and shifts in its rate and currency regime have outsized global implications.

Any disorderly adjustment, whether through sharper yen moves or further volatility in Japanese bond markets, has the potential to tighten global financial conditions and spill into equities and crypto alike. While this risk has not yet fully materialized, it remains unresolved and warrants close monitoring, particularly if global bond market volatility continues to rise.

Taken together, the macro backdrop is not outright hostile, but it is far less forgiving. Strong data, hawkish policy risk, and latent global liquidity pressures create an environment where excess is punished quickly. Crypto is adjusting to that reality.

Positioning, Sentiment, and the Path Forward

Sentiment reset sharply this week. Fear dominated flows, leverage was flushed, and defensive positioning increased meaningfully. Importantly, this was not a structural failure of crypto. It was a valuation and liquidity reset.

Oversold conditions are real, but they are not sufficient on their own to justify sustained upside. From here, markets will require confirmation through price repair, equity stabilisation, and macro clarity.

Bitcoin must reclaim the mid-$70k region to stabilise and ultimately retest higher levels. Ethereum must regain the $2,200 area to avoid prolonged underperformance. At the aggregate level, total market cap must reclaim $2.45 trillion to re-establish bullish structure.

Until then, rallies should be treated as tactical rather than structural.

Closing Thoughts

This week was painful, but it was also familiar. Crypto markets have always required periodic leverage resets to sustain long-term trends. What we saw was fast, mechanical, and unforgiving but not unprecedented.

The market is cleaner now. But it is not yet safe.

We are watching several things closely. Stabilisation in equities, particularly software and the Nasdaq will be important, as crypto continues to trade as a downstream expression of growth risk. Liquidity conditions, especially Fed net liquidity and global bond market volatility, remain critical inputs. Developments in Japan, where yield and currency dynamics have the potential to tighten global financial conditions, also bear close monitoring.

Patience, discipline, and respect for macro signals remain essential as we navigate the next phase.