Crypto entered the week under pressure, but the market held where it needed to.

BTC struggled to build momentum, alts lagged, yields moved higher, and Fed pricing shifted further hawkish. In that context, Bitcoin’s ability to defend the same support area we have been tracking for weeks is meaningful. The setup is still fragile, and this is not a clean risk-on environment, but unless macro deteriorates further, the case for a local BTC bottom continues to improve.

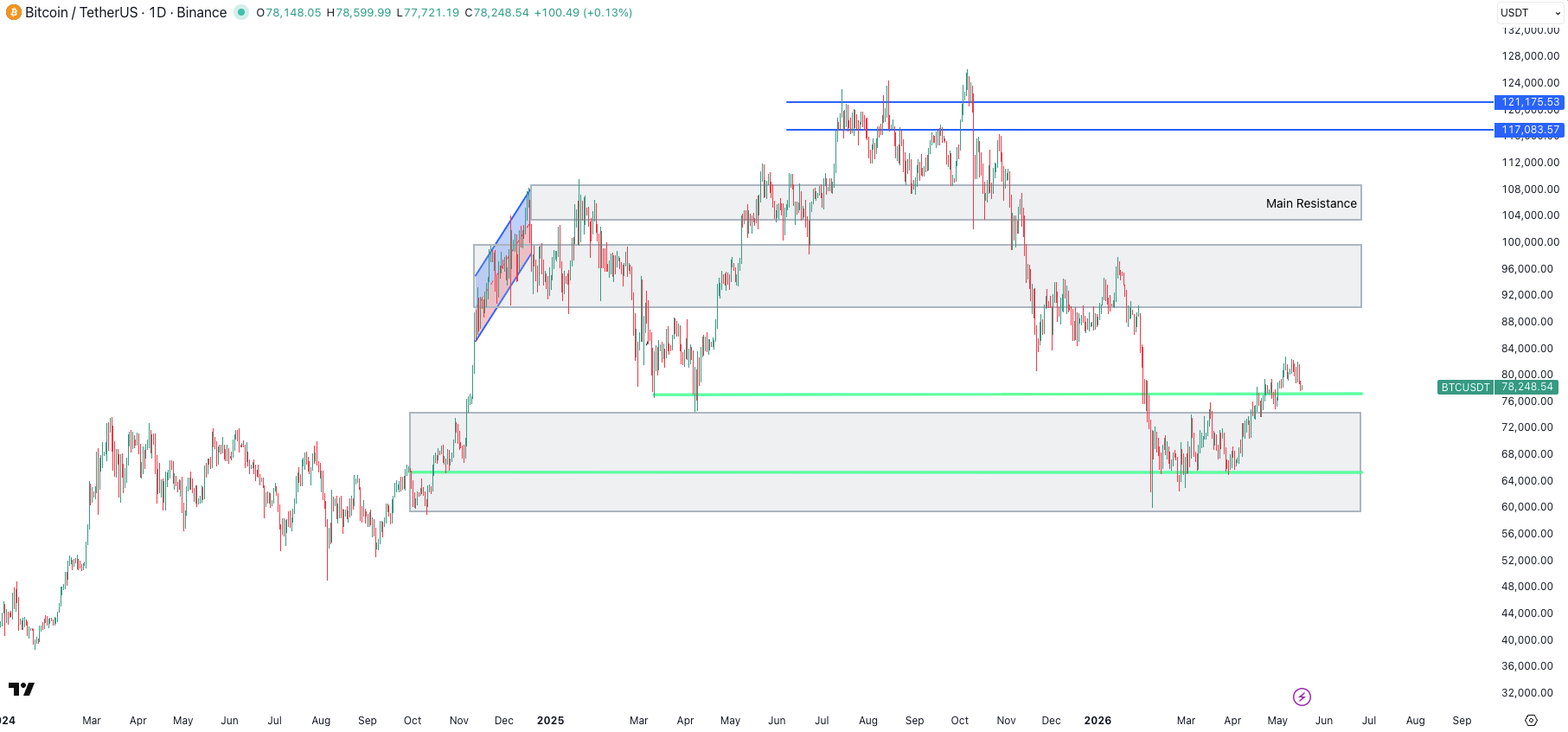

BTC is still the anchor. The key level remains $78k. Price pushed into the low $80ks earlier in the month, failed to extend, and has now pulled back toward the upper end of the major support zone. That is where bulls need to step in. As long as BTC holds around $78k, the market can continue to build a base. A reclaim of $80k would open the door to the mid-$80ks, where momentum can return quickly. Lose $78k decisively, and $65k–$68k becomes the obvious downside magnet again.

The larger structure is also unchanged. BTC still has heavy overhead supply above. $90k–$99k remains the first major resistance area, and $100k–$108k the next battleground. For now, the conversation is about whether BTC can keep holding support while macro pushes against risk assets.

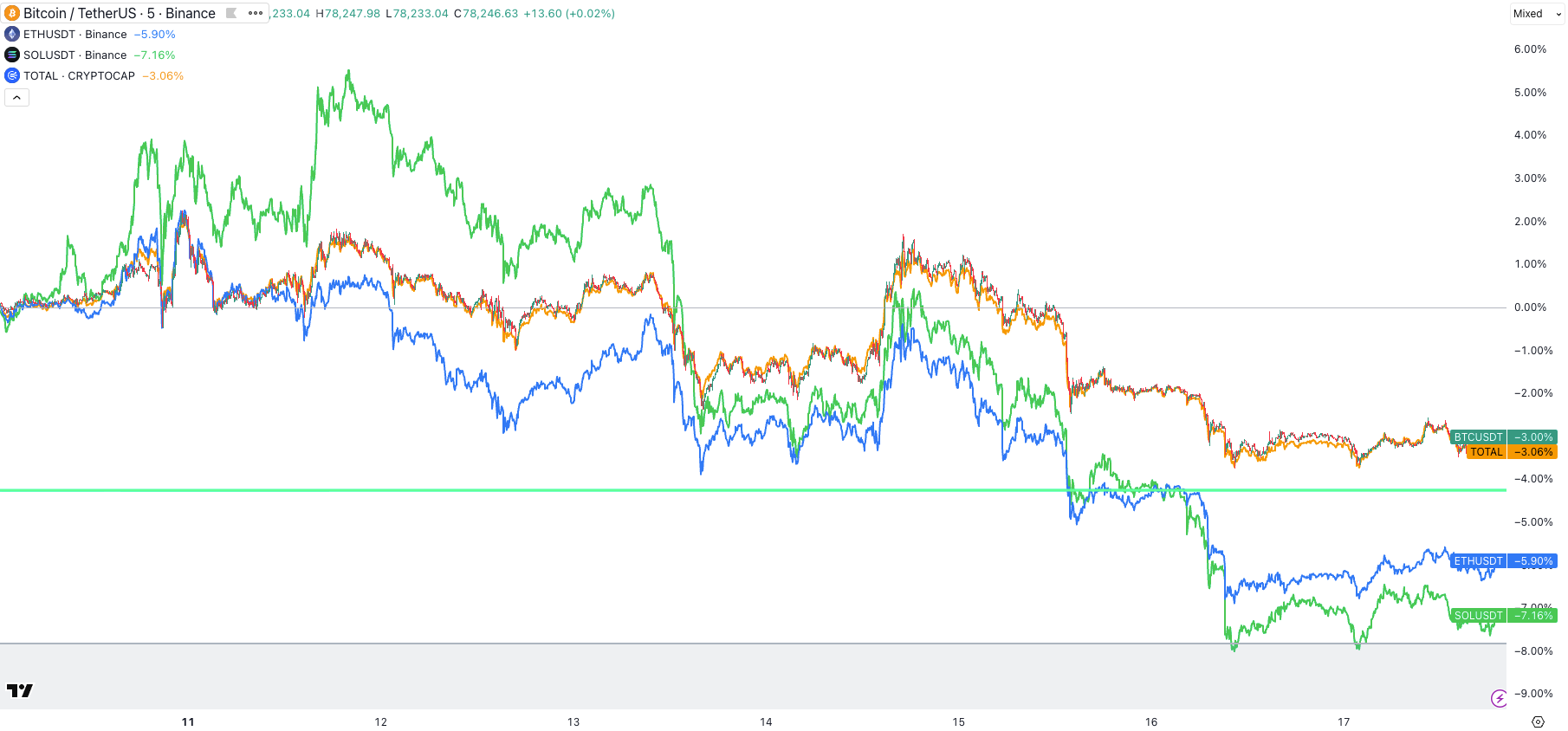

That is why this week was constructive, even if the price action did not feel good. BTC was down around 3% from the start of the week, roughly in line with total crypto market cap. ETH was weaker, down close to 6%, and SOL was weaker still, down more than 7%. This is not the tape of an aggressive risk-on rotation. It is defensive leadership. BTC remains the safest expression of the crypto trade, while alts are still waiting for permission.

But the alt setup is becoming more interesting. Altcoins have already taken a lot of pain. TOTAL3/BTC is sitting right on a long-term support shelf, and historically these levels tend to matter. Either alts break down violently from here, or they set up a strong reflexive bounce. Given BTC is holding support and has not made a fresh leg lower despite the macro pressure, the risk/reward for alts is improving tactically.

That does not mean we are calling for a new alt season. It means that if BTC has bottomed locally, alts should perform better on the upside. The first step is BTC stabilising above $78k. The second is reclaiming $80k. The third is macro not getting worse. If those boxes are checked, the alt complex can bounce hard from here.

The important word is “tactically.” This is not a structural all-clear. The market still has to deal with rising yields, sticky inflation, and a Fed being forced away from cuts. But crypto positioning already reflects a lot of fear. BTC has absorbed a difficult macro tape without breaking. Alts have lagged hard. Relative charts are sitting at support. That combination is usually where tradable rallies begin.

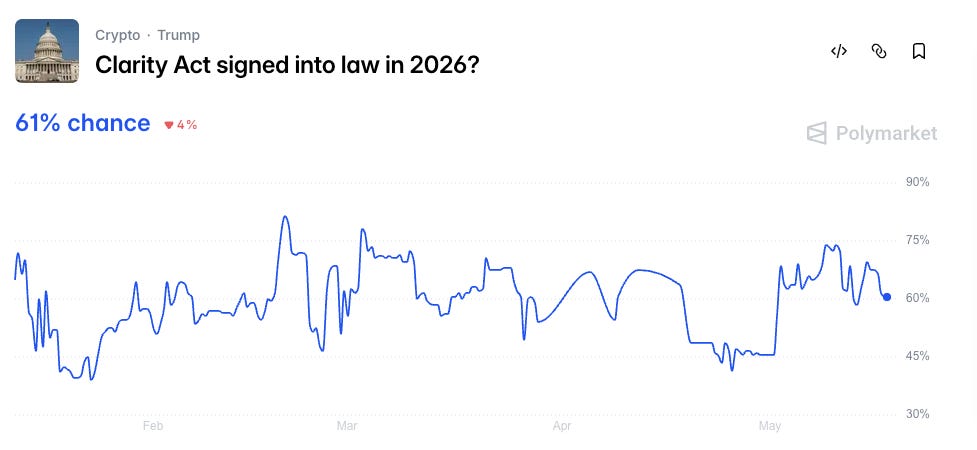

The other positive this week came from regulation. The Senate Banking Committee passed the Clarity Act in a 15–9 vote, sending the bill to the full Senate. Crypto has been waiting for clearer U.S. market structure for years, and the Clarity Act is one of the more serious attempts to draw lines between securities-style and commodities-style oversight. The market does not need every question solved tomorrow, but it does need direction. This vote gives it direction.

Still, we should not overstate it. A committee vote is not law. The bill still needs to clear the full Senate, and the politics remain messy. The Block highlighted comments from GSR’s legal chief, who put the odds of passage below 50%. Polymarket is more optimistic, with odds around 61% that the Clarity Act is signed into law in 2026. That gap is useful: lawyers are cautious, prediction markets are more bullish, and the truth is probably somewhere in the middle.

For crypto, the direction of travel is positive. Better market structure, clearer rules, and a more mature U.S. framework are all supportive for institutional capital over time. But regulation is not the main driver of the tape right now. It is a supportive background catalyst, not the thing deciding whether BTC breaks $80k or retests $65k.

Macro is still driving the bus.

Macro

The macro story became more uncomfortable this week.

U.S. data is running hot again, and American exceptionalism is back on screens. Not because the economy is perfect, but because the data keeps the Fed uncomfortable. CPI is hot. PPI is hot. Import prices are rising. Retail sales are holding up. The labour market has cooled from the post-pandemic boom, but it has not broken. That is the problem.

At the start of the year, the market was still dreaming about cuts. That dream is gone. The question is no longer “how many cuts does the Fed deliver?” The question is now “can the Fed avoid hiking if inflation keeps moving higher?”

That is a huge change.

The war and the Strait of Hormuz remain the centre of the inflation problem. The double blockade has dragged on long enough that the initial shock is starting to look less like a headline and more like a macro regime. Commodity, shipping, and supply chain experts continue to warn that the shutdown will eventually create broader supply shocks. Those warnings can feel stale because markets have short attention spans. But the longer the disruption lasts, the harder it becomes to dismiss.

Energy shocks are never just energy shocks. First they hit oil. Then gasoline. Then freight. Then import prices. Then producer prices. Then businesses begin passing higher costs through to consumers. At that point, the Fed cannot simply call it a one-time price-level adjustment and move on.

This is why the “transitory war shock” argument is too easy. Yes, part of the inflation impulse is caused by the war. Yes, if Hormuz reopens, some of that pressure can fade. But central banks do not just care about the first shock. They care about the psychology that follows. Once companies realise they can raise prices and consumers keep paying, inflation becomes harder to kill.

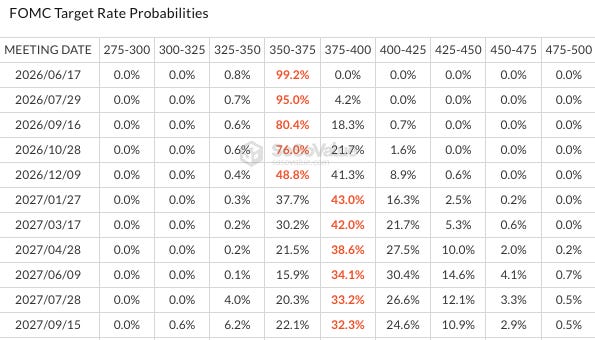

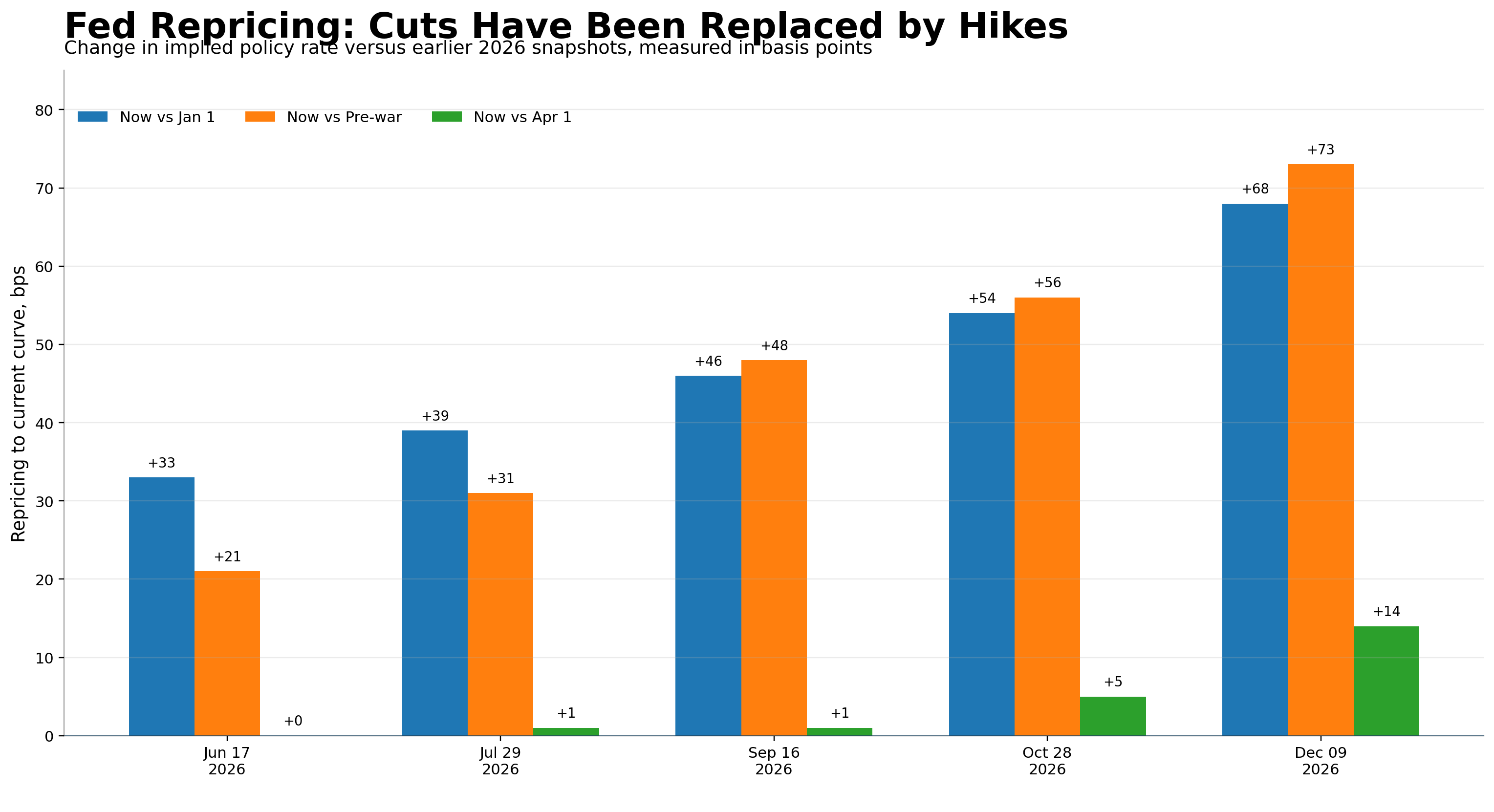

The Fed pricing chart captures the shift perfectly.

At the start of the year, the market was still pricing a cutting cycle. The January snapshot showed policy drifting lower through 2026. By mid-February, that path had already moved higher because the labour market refused to crack. By April 1, after the war premium started to matter, the easing cycle had largely disappeared. The market had moved from “cuts are coming” to “maybe the Fed just stays on hold.”

Now the red line is above all of them.

That is the big macro story this week. The market has gone from pricing cuts to pricing hikes. Kevin Warsh taking the helm of the Fed makes the setup even more interesting. The crazy reality is that his first move could be a hike, not a cut. That is not necessarily the base case yet, but it is no longer a tail risk that can be ignored. If inflation keeps rising and the labour market stays in equilibrium, Warsh and Waller could both sound hawkish by mid-summer. A December hike is now a realistic market conversation.

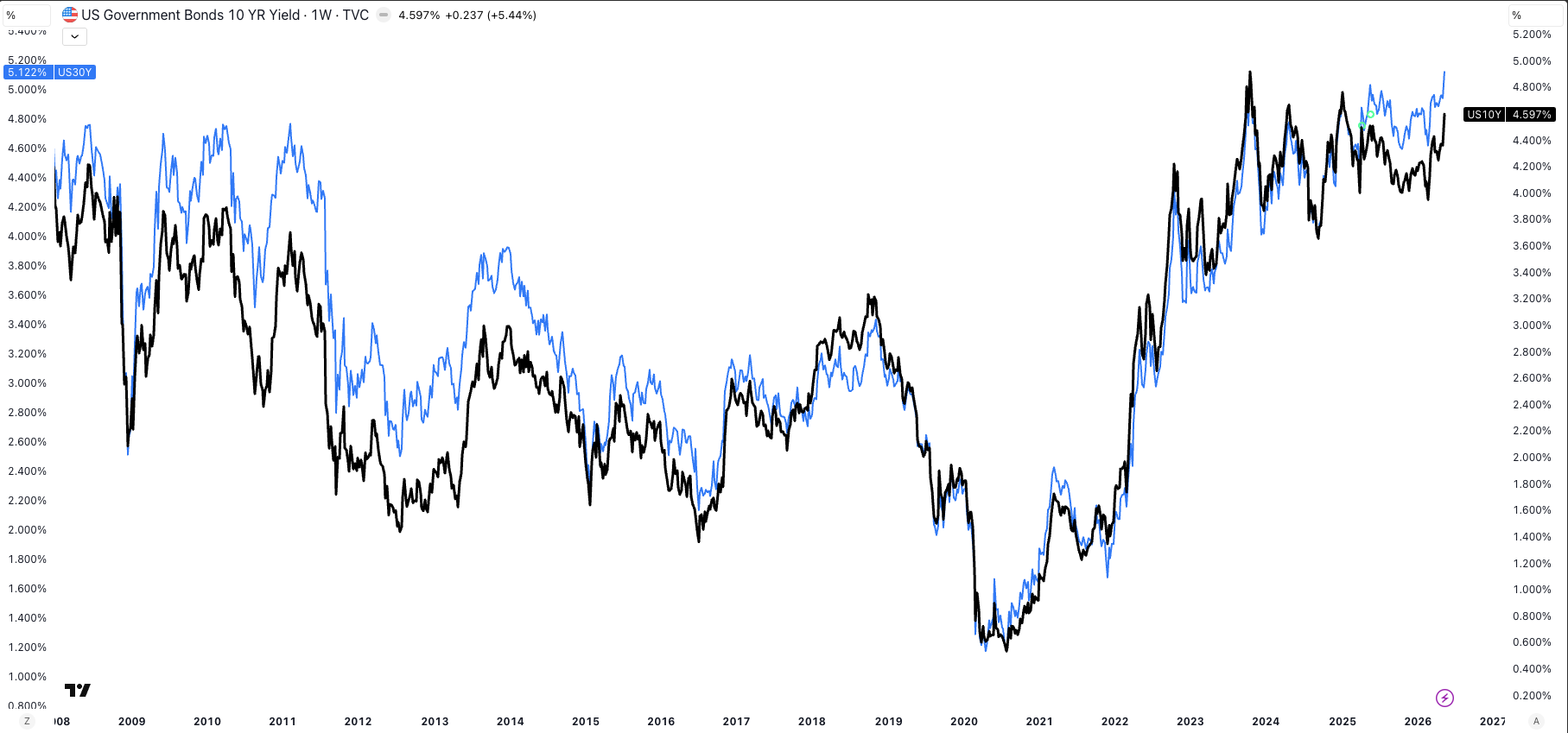

The bond market is already taking notice. The 10-year and 30-year yields are pushing higher again, with the long end doing real tightening work. Higher long-end yields pressure equity multiples, tighten financial conditions, and make speculative assets harder to own.

The AI capex boom is the other side of the macro story. It continues to support equities, keep some regional labour markets tight, and maintain the American exceptionalism narrative. The hyperscalers are still spending aggressively. Data centres, power, chips, cooling, construction, and infrastructure are all absorbing resources. That keeps parts of the economy hotter than they otherwise would be.

So the market is stuck between two forces. On one side, AI capex and resilient U.S. growth keep risk appetite alive. On the other side, inflation, energy, shipping, and higher yields are pulling the Fed more hawkish. Stocks have been outperforming, but the move could be running out of steam. If yields keep rising, eventually the discount-rate math starts to matter again.

For crypto, the macro filter remains simple. If yields stabilise and Fed pricing stops moving hawkish, BTC can hold support and alts can bounce. If oil pressure eases and Hormuz moves toward resolution, risk assets can breathe. If inflation cools in the next set of data, the market can return to the idea that the Fed is on hold rather than preparing to hike.

But if the opposite happens, downside risk returns quickly. Another extension of the Hormuz disruption, another hot inflation print, another move higher in the long end, or another repricing toward Fed hikes would make the crypto bounce much harder to sustain.

That is why we should not confuse a local bottom with a solved macro problem. BTC can bottom here. Alts can outperform on the upside. The Clarity Act can improve the medium-term regulatory outlook. All of that can be true while the bigger macro backdrop remains dangerous.

Looking Ahead

Next week is about confirmation.

BTC has done enough to keep the tactical bounce alive, but not enough to declare victory. The level to watch is still $78k. Hold above it, and the local bottom case remains intact. Reclaim $80k, and the path toward the mid-$80ks opens up quickly.

That is where alts should start to work. They are washed out, TOTAL3/BTC is sitting on long-term support, and positioning already reflects a lot of fear. The alt trade does not need perfect macro. It just needs BTC to stop going down.

But macro still has the final say. If yields keep pushing higher, oil stays firm, or Fed pricing moves further toward hikes, the bounce becomes much harder to sustain. A clean loss of $78k would put $65k–$68k back in play.

So the playbook is simple: hold $78k and reclaim $80k, and we lean into the bounce. Lose $78k, and we respect the risk of another leg lower.

The market has earned a bounce.

It has not earned complacency.