Last week was not a pullback. It was a liquidation.

Total crypto market cap fell 12.8%. BTC was down 13.7%, ETH down 19.3%, and SOL down 20.8%. Total market cap now sits around $2.11T, down 52% from the October ATH and 30% from the 2021 ATH. Ex-stables, the drawdown is even worse: -56% from October and -40% from the 2021 high. The reason this matters is simple: TOTALES is now sitting directly on support.

If this level breaks, the next clean support is around $1.4T. That would take us back to November 2023 levels and effectively reset the entire post-2023 crypto beta trade.

The theme this week is not “all clear”. It is bottoming process. The market is oversold enough for violent reflex bounces. BTC and SOL are pinned to the floor of their one-year value areas, RSI is washed, and reversal trend is flashing. This is the type of zone where bounces usually start. But bounces are not bottoms by default.

The macro tape is still hostile, flows are still poor, and the institutional bid that carried much of this cycle has clearly weakened. We are no longer in the middle of the range. We are at the floor. That does not mean the low is in.

It means the market is finally trading where risk/reward starts to change.

Crypto

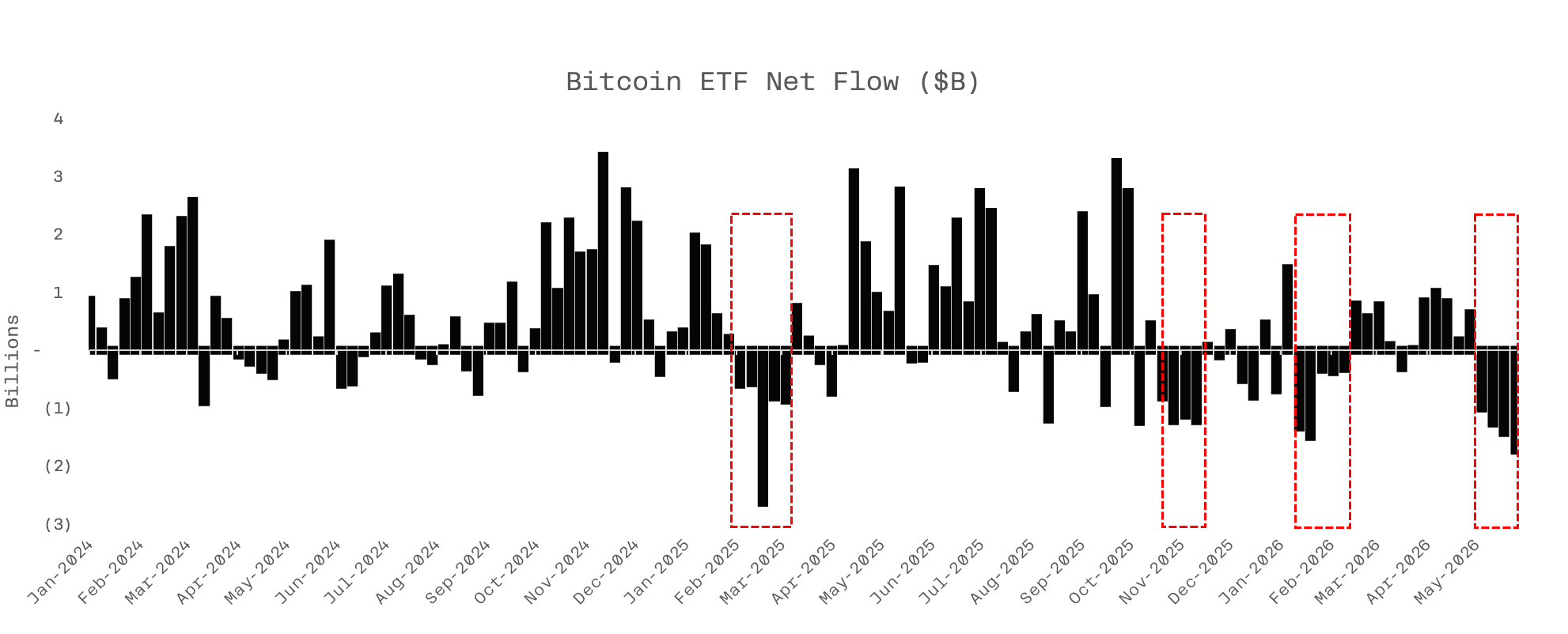

The most important thing in crypto this week was not just the price action. It was the flow picture. One distinction matters. U.S. spot bitcoin ETF outflows worsened from roughly $1.0bn in the week of 11–15 May to $1.26bn, $1.42bn and then $1.72bn in the week of 1–5 June. That is not noise. That is persistent de-risking.

The structural bid is no longer absorbing supply in the same way. For most of this cycle, the ETF bid was the cleanest expression of demand. When that bid turns into repeated weekly outflows, the market starts to feel heavy. Not because there are no buyers, but because the marginal buyer has stepped back.

Strategy is the other pressure point. The 30 May / 1 June disclosure showed that between 26 and 31 May, Strategy sold 32 BTC for roughly $2.5M. It also sold around 801,994 MSTR shares for $128.3M in net proceeds, issued no preferred stock during the period, and ended May with 843,706 BTC plus a $900M USD reserve.

So the answer to the most important question is nuanced. Capital markets were still open to the common-equity ATM. But the BTC treasury itself was a net source of cash at the margin, not a buyer. That matters because the entire market has spent years treating Strategy as a one-way structural bid. Sell equity. Issue preferred. Buy BTC. Lift NAV. Repeat. This week showed something different.

The sale was tiny in size, but large in signal. If Strategy sold more, the move makes sense. The market is pricing a shift from permanent buyer to potential marginal seller. If they managed to tap capital markets and buy more, that is neutral. If they were buying while BTC still sold off this hard, then flows are strongly against BTC.

STRC is where the stress is showing up.

Strategy’s STRC now trades below par, with the latest price around $93.40, an effective yield of 12.31%, and a variable annual dividend rate of 11.50%. This is a security designed to trade around the $100 stated amount. When something engineered to hug par is sitting materially below par, the market is telling you the funding flywheel is under strain.

That does not mean crisis. It means the marginal source of easy crypto-linked financing is less powerful than it was.

Technically, the setup is much cleaner than the tape feels.

BTC, ETH, SOL are both pinned to the floor of their one-year value areas. BTC is around $60k. ETH around xxx SOL is around $61. RSI is in the mid-teens fresh trend reversal setups. This is exactly the kind of place where reflex bounces start.

But oversold is not the same as repaired. All are still below major moving averages. Volume thins quickly below spot. Any near-term strength should be treated as tactical until the market proves otherwise.

For BTC, the map is simple.

Zone 1: $59k–$61k: This is the first accumulation area and the current floor.

Zone 2: $56k–$57.5k: This is where the air pocket starts.

Zone 3: $53k–$55k: This is the capitulation flush / deep-value zone.

If BTC loses $60k and then $59k, the lack of volume support below means the move can accelerate quickly.

For ETH, the support zones are:

Zone 1: $1,500–$1,650: Current support. If ETH is going to stabilize without a full flush, it probably has to do it here.

Zone 2: $1,250–$1,425: The next obvious support pocket if $1,500 fails.

Zone 3: $900–$1,050: The deep-value washout area.

Macro

Macro is not yet giving crypto a clean tailwind. The latest official U.S. inflation data show core PCE at 3.3% year on year in April, up from 3.2% in March, while headline PCE rose to 3.8% from 3.5%. The Dallas Fed’s trimmed-mean PCE measure is still lower at 2.3%, but that gap is precisely why the market remains edgy: if underlying inflation measures keep firming, the disinflation story gets harder to defend. At the same time, Kevin Warsh has just taken office as Fed chair, and the next FOMC meeting is scheduled for 16–17 June.

The growth side of the macro tape also pushed in a hawkish direction. U.S. nonfarm payrolls rose by 172,000 in May, well above expectations, while unemployment held at 4.3%. That is one reason equities sold off hard into the weekend and why Warsh’s first meeting now looks more like a risk event than a relief event. Put simply: inflation is not cooling fast enough, growth is not weakening fast enough, and markets have had to reprice the chance that rates stay restrictive for longer.

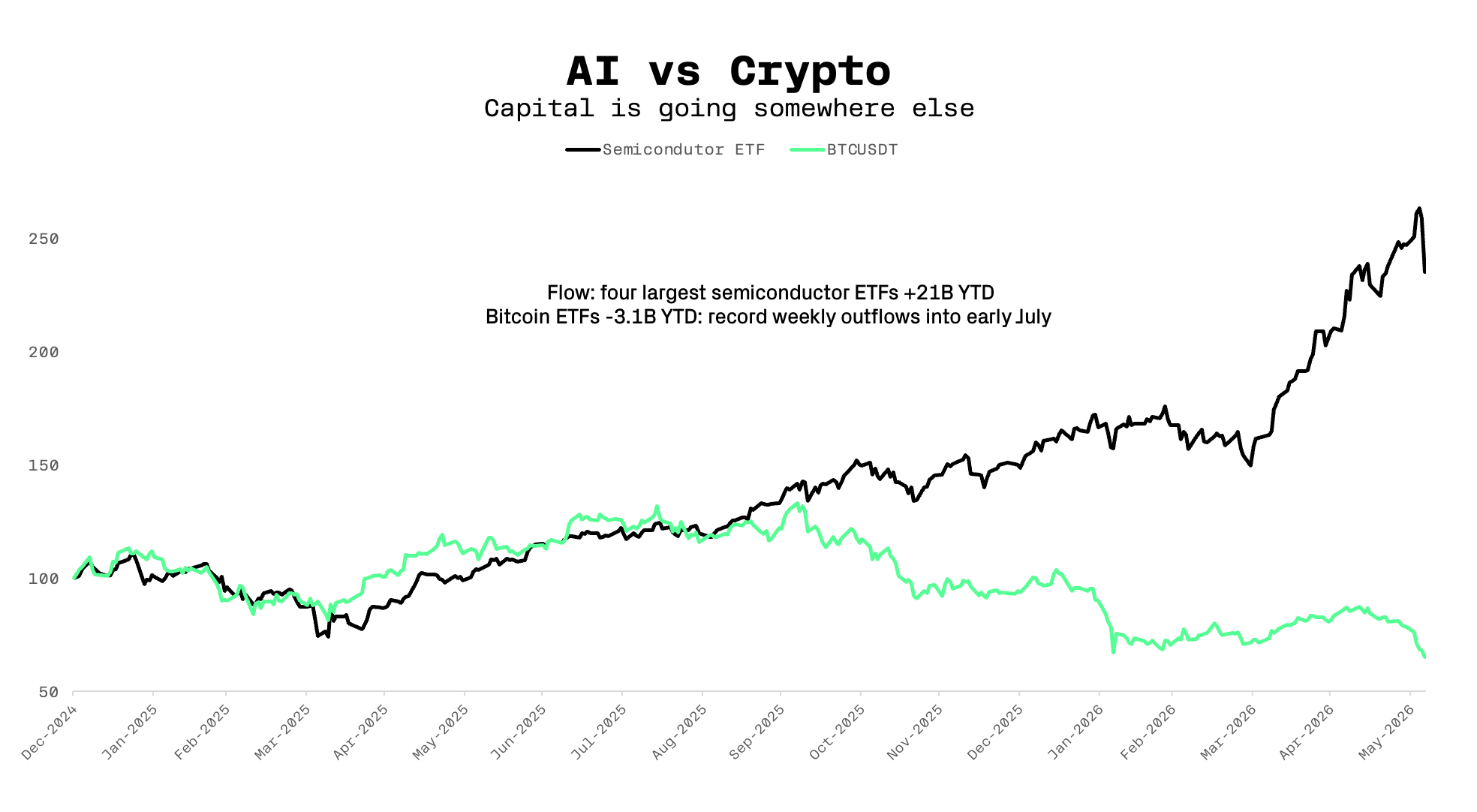

That repricing hit growth equities directly. S&P 500 posted a weekly decline after nine straight weeks of gains, while Friday’s selloff was driven by stronger jobs data and a hit to semiconductors after Broadcom disappointed. Broadcom left its fiscal 2027 AI revenue forecast unchanged and missed second-quarter revenue expectations, sparking a broader chip selloff. In other words, the macro backdrop is tight enough that “good but not perfect” is suddenly not good enough for crowded AI winners.

The AI trade

The bear case on AI financials is no longer fringe with key focal points around cost, tokens and monetisation rather than growth. The key point is simple: tokens have become the revenue engine for model providers, but they are also exposing how expensive AI usage is for customers. A growing backlash from enterprise buyers who are burning through token budgets without a clear line of sight to business value, while Google has already begun pitching Gemini as a cheaper option for firms trying to manage spend. ROI on AI investment remain hazy, daily token costs can exceed human labour for some tasks, and boards are likely to impose much tighter financial discipline.

That fits the broader chip-cost story as well. Surging memory prices are now feeding “chipflation”, pushing manufacturers toward harder choices on pricing, margins and component use. Put differently, the cure for very high AI costs is likely to be efficiency, not unlimited spending. That does not kill the AI story. It changes the market’s willingness to pay peak multiples for every name leveraged to it.

SpaceX is the immediate liquidity event hanging over that trade. The IPO has been priced at $135 a share, is targeting a $75bn raise at a $1.75tn valuation, and is expected to be listed 12 June. The deal is 2x oversubscribed. Damodaran’s latest post is a useful counterweight: he argues that the selling machine around this IPO will be intense, that the equity story will be marketed partly as an AI vehicle, and that investors should pressure-test the plausibility of the numbers rather than just buy the narrative.

SpaceX is not the only draw on capital. Anthropic has now confidentially filed for a U.S. IPO, while OpenAI is also preparing to file. The combined demand for capital from SpaceX, OpenAI and Anthropic is likely to be large enough to disrupt flows across public markets.

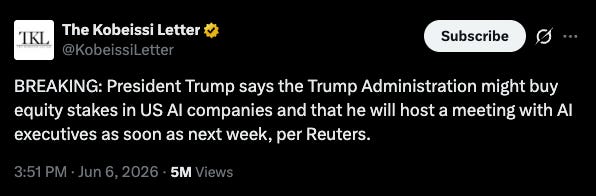

There is one possible offset. Reports has started to circulate that senior U.S. officials have held preliminary discussions about the government potentially taking stakes in AI companies, and Trump said his team would look into the idea. AI policy headlines might help sentiment at the margin for a few days, but they are not the same thing as a durable fix for stretched positioning and rising cost anxiety. As we’ve stated many times in the past, if/when equities get a stronger correction, crypto wont be able to withhold the further downside pressure.

Why this still looks like a bottoming process

The case for a crypto bounce is becoming stronger, even if the case for a durable low is not there yet. BTC having one of its worst weekly drop since late 2022, while ETF outflows have accelerated and capital continues to been rotating into AI. Bitcoin’s relationship with the S&P 500 has flipped deeply negative as AI equities continue to attract money while crypto lags. That is exactly the kind of dislocation that can produce sharp, tradable mean reversion once the forced sellers are done.

So the working view should be: massively oversold, probably due a bounce, but not obviously the final low. That means patience and staggered spot buying make more sense than swinging for the fences. The confirmation signals to watch are straightforward: skew settling down, heavy volume into support followed by reversal, ETF redemptions easing, and no further unpleasant surprises from Strategy’s treasury or STRC. Until those things improve, treat the setup as a bottoming process, not a confirmed bottom.

What to watch this week

The immediate line in the sand is still BTC $59k–$61k. Hold that, and the market can stage a sharp relief move simply because positioning and sentiment are so washed out. Lose it, and the air pocket into $56k–$57.5k opens fast. The same logic applies to SOL $60–$63, with $54–$56.5 the next destination if support fails, and to ETH $1,500–$1,650, where failure would likely drag the market towards $1,250–$1,425.

The checklist for the week is clear. Watch daily U.S. spot ETF flows. Watch Strategy’s purchases page and any fresh SEC filings for evidence of renewed BTC buying or further treasury sales. Watch whether STRC can stabilise near par or whether it keeps drifting lower. Watch SpaceX pricing and listing developments, and watch whether Anthropic/OpenAI headlines keep pulling speculative cash into AI instead of back into crypto. All of that sits in front of Warsh’s first FOMC on 16–17 June, which is now shaping up as the next major macro hazard.

The bottom line is simple. Crypto is getting close to deep value in a number of important names, but the market has not yet earned the right to call the all-clear. Start buying the better zones slowly. Respect the air pockets. Expect a bounce before a clean trend turn. And if the tape does not improve on flows, be ready for one more flush before the real reset is complete.