Groundhog‑day markets, but with one key extension: the geopolitical stress has not faded, and the Strait of Hormuz remains the transmission channel. With the waterway still effectively shut and mine risks reported in the corridor, the macro question is no longer “is growth slowing?” so much as “does energy inflation stay embedded long enough to change the rate path?”.

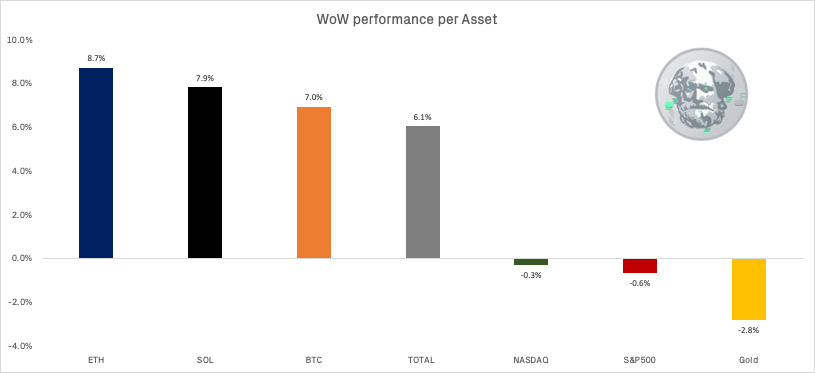

Crypto’s tell was resilience. Bitcoin traded back into the low‑$70k region and Ethereum reclaimed $2k, even as gold logged another weekly decline and markets pushed expectations for rate cuts further out. This is the first time in a while that “war + higher‑for‑longer risk” has co‑existed with a bid for BTC/ETH rather than a liquidation.

Crypto

Bitcoin’s recovery looked more like repair than mania: daily closes show BTC grinding higher through the week, and broader market coverage noted trading above $73k on Friday. The tone matters because it suggests demand was present across the week, not just concentrated in one squeeze candle.

Flows have started to validate price. Reporting on spot bitcoin products pointed to a solidly positive week, with roughly $763m of net inflows into ETF. Directionally, this is the important development: a return to accumulation in the face of a messy macro backdrop.

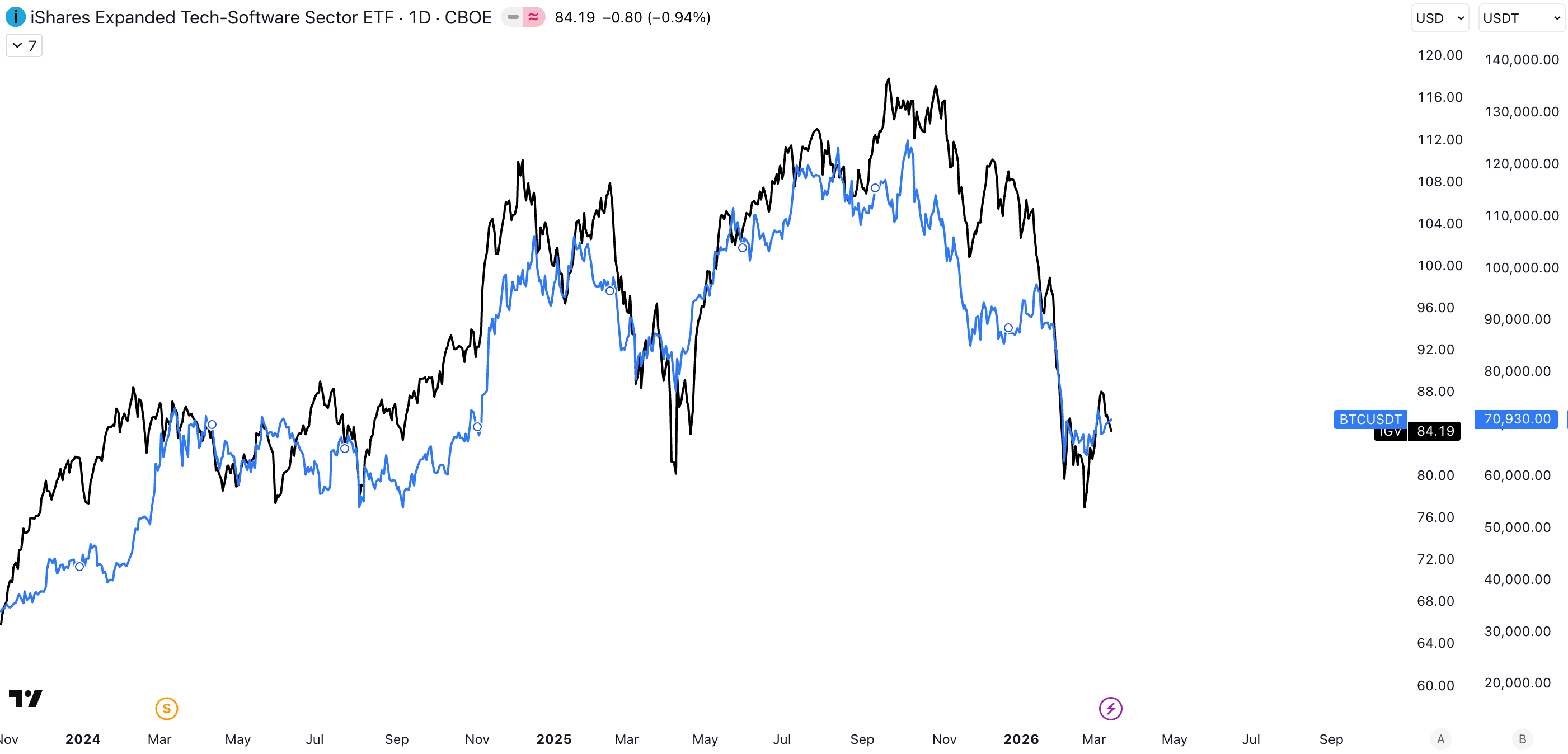

The cross‑asset wrinkle to watch is decoupling from software/growth proxies. Over the same window that bitcoin was recovering toward $70k+, the IGV software ETF stayed weak in daily data. One month will not de‑correlate a multi‑year tape, but it is the first clean hint in a while that bitcoin can trade as an “alternative asset” in an oil‑shock regime rather than purely as high‑beta tech.

Broader crypto also improved modestly. The “TOTAL3ES” series (crypto market cap excluding BTC, ETH and stablecoins) was up mid‑single digits on the week, consistent with a “risk appetite stabilising” narrative rather than a full‑blown alt season. The important nuance is that by excluding stablecoins, this series tries to isolate whether non‑stable risk capital is actually rotating into smaller assets.

Currently trading in 360-480B range, back to pre-election levels.

ETH and the return of yield

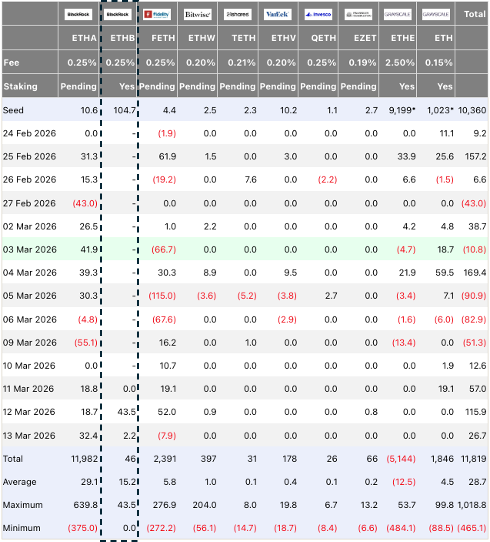

Ethereum gained a genuinely new leg this week: BlackRock launched the iShares Staked Ethereum Trust ETF (ETHB), designed to provide spot ether exposure while potentially generating income by staking a portion of the underlying. This is not just “another ETH ETF”; it brings native Ethereum yield into a conventional brokerage wrapper.

Two details matter. First, the product’s fee structure includes a temporary waiver (0.12% for the first 12 months on the first $2.5bn of assets, then 0.25% thereafter). Second, it is explicitly positioned as a way to participate in staking rewards without the operational burden of doing it directly. In plain terms: ETHB is trying to sell “carry + beta” in one ticker.

The longer‑term implication is narrative, not immediate price: once staking yield is normalised inside broker accounts, “holding ETH” becomes easier to frame as owning a yield‑bearing digital asset, rather than purely as a high‑beta tech proxy. Over time, that can change the marginal allocator’s willingness to hold through drawdowns particularly if the alternative is cash with a delayed path to policy easing.

Geopolitics and the oil shock

The macro mechanics are simple: if Hormuz is unsafe, the market carries an oil risk premium. Reporting this week described mine‑laying activity by Iran and multiple merchant‑ship incidents in and around the strait, with tanker traffic largely stopping. Even before you debate “how long”, the market must price “how bad” because reopening and re‑insuring the corridor is not instantaneous.

Scale is the point. Supply impacts measured in the high single‑digit millions of barrels per day and Hormuz represent roughly a fifth of global oil supply. That is why the tape has felt “option‑like”: violent repricing on each new headline, followed by fast mean‑reversion when participants are forced to re‑weight probabilities.

At the time of writing, markets have yet to react to a ton of new events, including US strikes on Kharg Island and President Trump's global call to militarily open the Strait of Hormuz. However the 24/7 market on Hyperliquid is indicating a price action over the weekend.

The policy response is now matching the magnitude. The International Energy Agency said more than 400 million barrels of strategic reserves will begin flowing soon, a record‑sized draw designed to combat price spikes. Reserves can buy time, but they do not clear a blocked chokepoint, meaning the oil path, and therefore the inflation path, still hinges on reopening the strait.

However, the shock goes beyond just oil. LNG, less fungible than oil, may transmit disruption faster; that diesel, jet fuel and fertilisers follow close behind; and that downstream products like plastics can create negative supply‑chain surprises. Refinery and chemical‑plant shutdowns are not like flicking a switch, restarts can take a week or more, which creates inertia in downstream shortages once facilities begin to go offline.

Macro

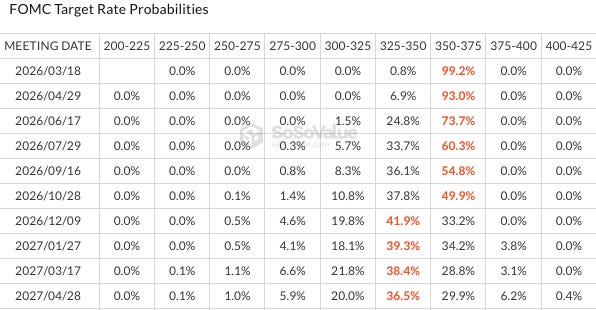

This week’s macro gate in the United States is the Federal Reserve meeting on 17–18 March, which is one of the meetings associated with a Summary of Economic Projections. The base case is a hold; the real information is in inflation messaging and in how the dots respond to an oil shock that is already reverberating across assets. Market‑implied probabilities for the March decision remain overwhelmingly skewed to “no change” (often quoted around ~99% depending on data vendor).

Rates markets have moved towards “higher for longer”. As of Friday, futures pricing implied slightly less than a standard 25bp cut by December, down from roughly two cuts before the conflict escalated. Major bank forecasts have followed the tape: Goldman Sachs now expects the first cut in September (and keeps December as a second), while Barclays has also delayed its first‑cut call and talks in terms of fewer total cuts.

A subtle but important shift is that “hike talk” has returned as a tail outcome. It remains a low‑probability scenario, but the mere discussion widens the distribution for real rates and crypto historically struggles when the market has to price that kind of asymmetry.

Liquidity and the plumbing

Even in a war tape, liquidity plumbing still matters, because it tells you whether volatility is likely to trigger forced selling. A widely used proxy for “system liquidity” is Fed net liquidity.

Fed Net Liquidity = Fed total assets minus the Treasury General Account (TGA) minus the overnight reverse repo facility (ON RRP).

The key message for this week: nothing here is flashing “liquidity accident”.

Fed total assets rose week‑on‑week to about $6.65tn in the latest available weekly data. The TGA weekly average was about $838bn. ON RRP continues to sit near effectively zero in size terms, removing what used to be a major “liquidity release valve” from the equation.

More supportive for risk is the higher‑frequency cash‑flow picture. U.S. Department of the Treasury daily data show large swings in the TGA balance (for example, a closing balance around $809bn on 12 March after an opening balance above $862bn on 11 March). When the TGA drains, it mechanically adds liquidity back into the private sector the “TGA coming into the market” effect referenced in risk commentary.

Our Take

The regime hasn’t changed: oil is still the macro variable. As long as Hormuz remains disrupted, energy prices continue to feed directly into inflation expectations and rate pricing.

What’s notable is crypto’s reaction. Despite the same macro backdrop, geopolitical stress and rate cuts pushed further out, BTC and ETH stabilised and moved higher. Improving ETF inflows and the introduction of staking-enabled ETH products are beginning to provide structural support, while liquidity conditions remain broadly stable as TGA flows add cash back into the system.

The next immediate gate is this week’s Fed meeting (17–18 March). A hold is fully expected; the real signal will be in how policymakers frame oil-driven inflation persistence.

Technically the levels are clear:

BTC: reclaim and hold $72–74k to reopen upside; otherwise the market likely remains stuck in the $60–74k repair range.

ETH: holding $2k keeps the structure stable, while $2.2–2.4k is the key reclaim zone.

If oil stabilises, crypto likely continues repairing. If the Hormuz shock intensifies, inflation and real rates will dominate again.