Crypto had another week where the headline price action said less than the plumbing underneath. BTC traded heavy, ETH continued to look like the complex’s weak duration leg, and SOL remained the cleaner expression of tactical beta. That part is not new. What is new is that crypto’s market structure is moving forward at the same time that macro is becoming more demanding. The rails are improving, the products are coming onshore, stablecoins are becoming more relevant to Treasury demand, and yet price is still struggling to fully respond.

That is the important tension this week. Crypto is maturing into a more institutional market, but it is doing so inside a world where capital has a higher hurdle rate, the U.S. Treasury needs more buyers, and every asset class is competing for balance sheet.

Last week was about the US-Iran process as a rates trade. This week is about something slightly different: who absorbs all the paper? Treasury paper, AI capex paper, stablecoin collateral, crypto leverage, and risk assets all sit inside the same balance-sheet system. When balance sheet is abundant, everything can work at once. When balance sheet becomes more selective, dispersion replaces beta.

Crypto

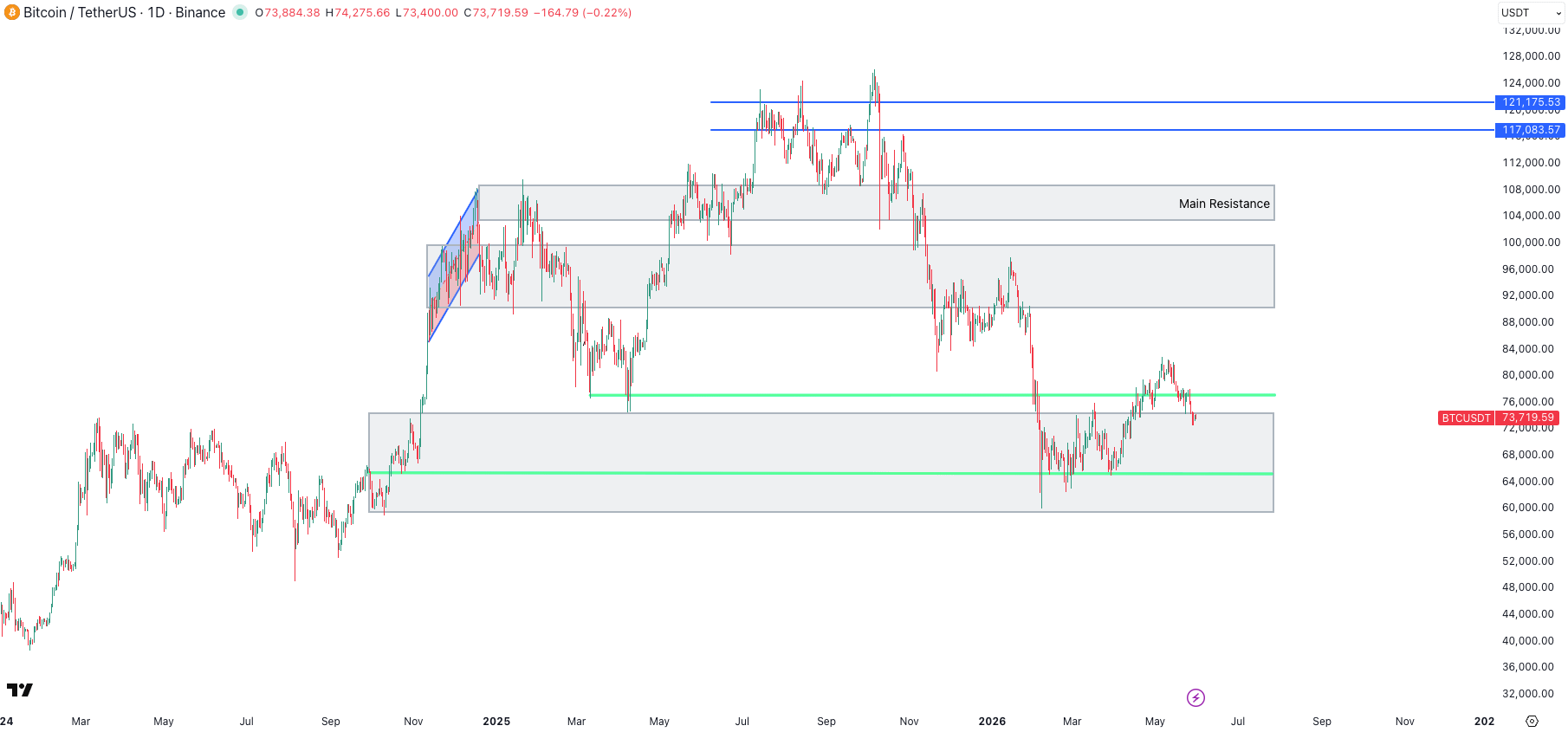

BTC remains the asset the market trusts most, but it is not trading like a clean breakout asset yet. That distinction matters. It can be the strongest asset in crypto and still not be ready to lead a broad risk cycle.

The reason is simple: BTC is now sitting between two stories. The structural story is strong. ETF ownership, treasury adoption, reduced exchange float, and institutional familiarity all continue to improve. But the tactical story is still messy. When real yields stay elevated and the long end refuses to behave, BTC does not trade like a pure monetary debasement hedge. It trades like high-quality macro collateral with no yield.

That is still much better than being a low-quality altcoin, but it is not the same as being immune.

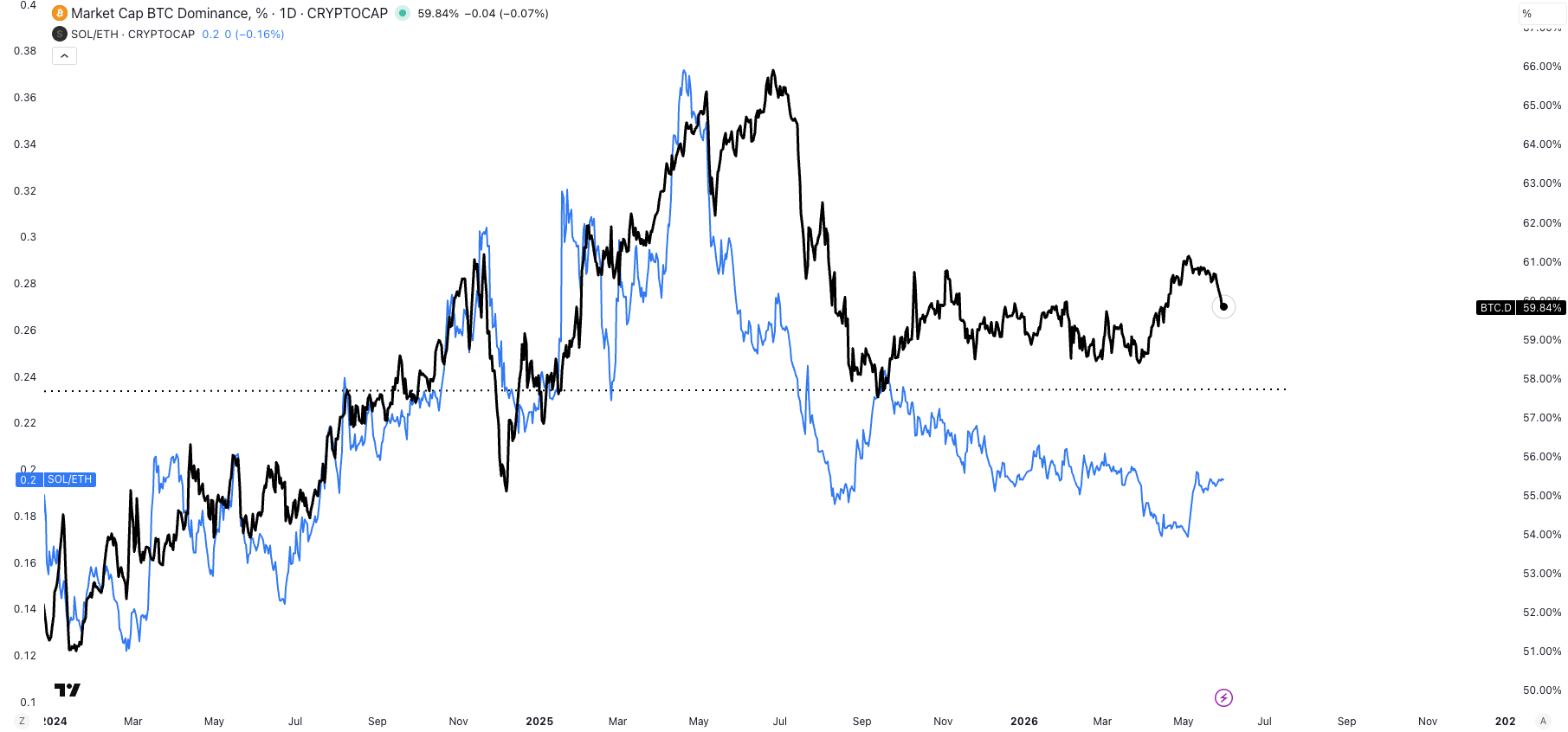

ETH remains the problem child. It is not that Ethereum has no activity. It is that the market is not paying for that activity right now. ETH still feels like an asset caught between narratives: too mature to trade like a reflexive growth chain, too fragmented to trade like clean monetary premium, and too dependent on lower macro volatility to lead. If BTC is crypto’s collateral asset, ETH is still trading like crypto’s operating system equity. In this environment, collateral is being rewarded more than operating leverage.

SOL remains the opposite. It is easier, cleaner, faster beta. When the market wants risk, SOL still gets reached for first. When the market de-risks, that same simplicity becomes a liability. So the playbook remains tactical rather than structural: SOL can outperform hard in a relief rally, but it is not the asset you want to hide in if yields turn higher again.

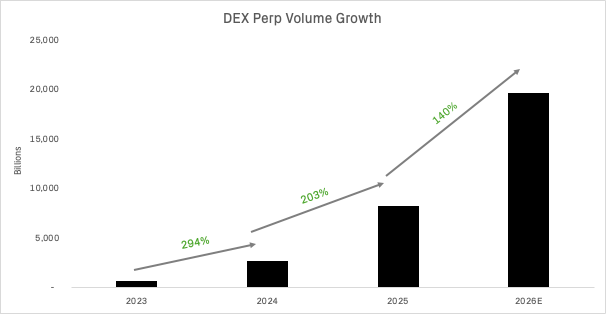

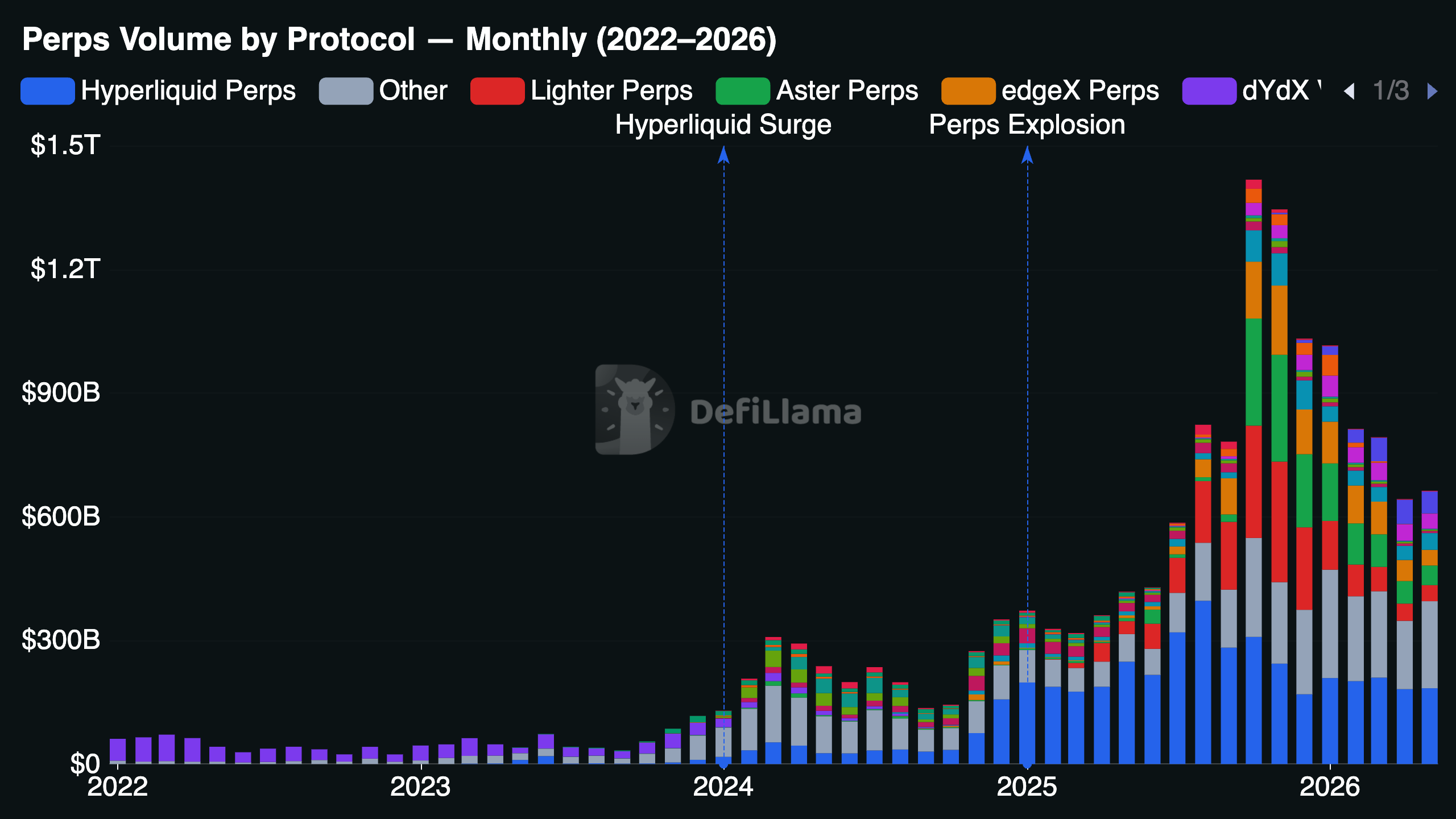

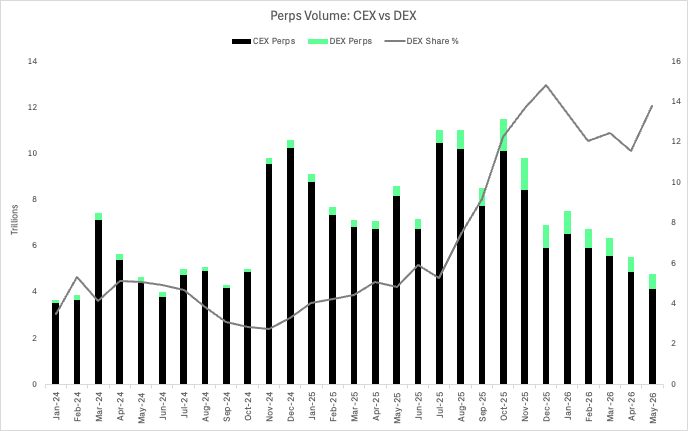

The more important update is market structure. Coinbase and Kalshi are bringing regulated perpetual crypto futures to U.S. investors, moving one of crypto’s most important offshore products into domestic regulated venues.

Perpetual futures onchain has increased >200% in both 2024 and 2025 and in 2025 alone about $8.2 trillion of volume alone.

This means crypto leverage is slowly being pulled out of offshore opacity and into regulated collateral systems. The onchain perp market reached as high as 15% of total CEX perps.

The irony is that this happens at the exact moment when leverage is becoming more expensive everywhere else. The bullish read is structural: better venues, deeper liquidity, more institutional comfort. The cautious read is cyclical: regulated leverage still needs balance sheet, and balance sheet is no longer free.

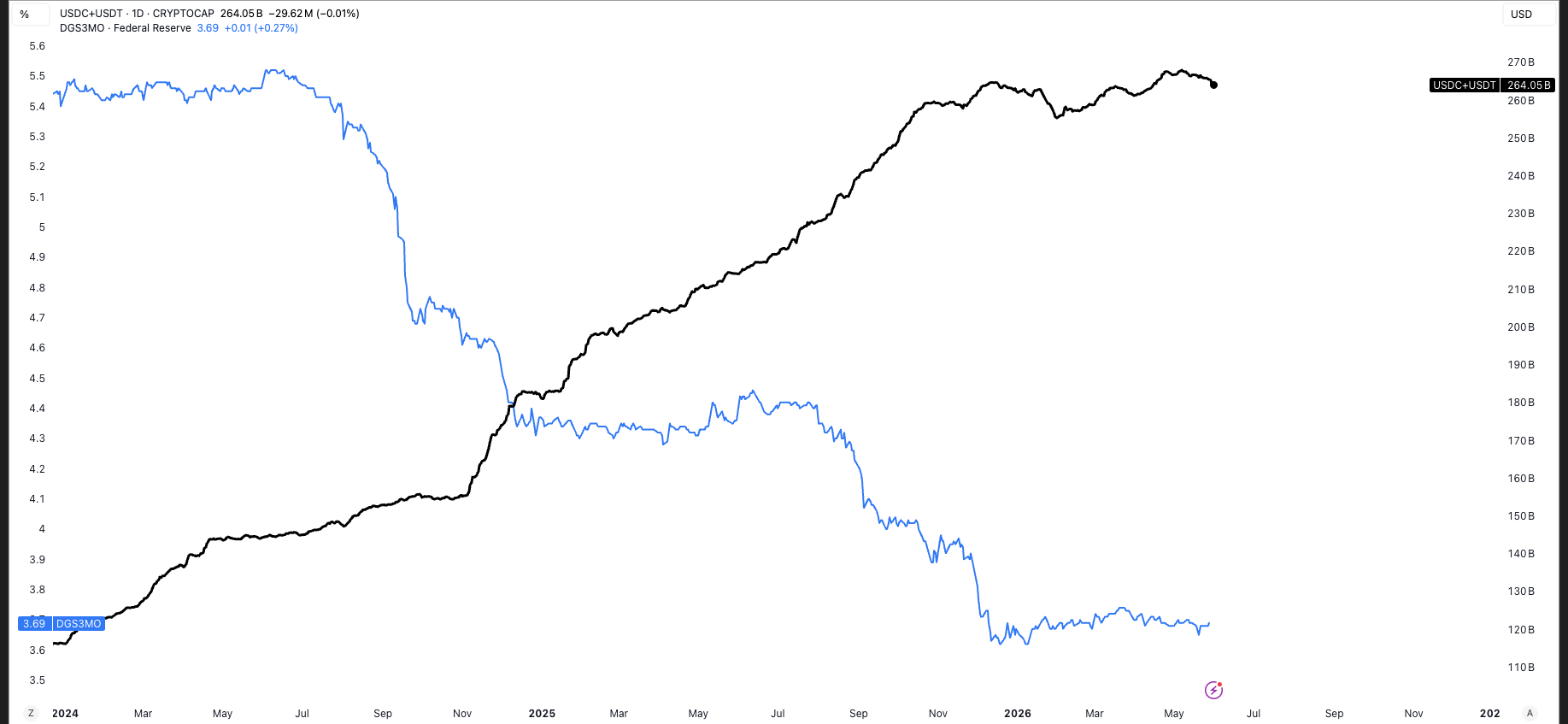

Stablecoins sit in the same bucket. They are no longer just crypto casino chips. They are becoming a shadow demand channel for short-duration U.S. government collateral. Q1 2026 data indicated that Tether holds $141 billion of U.S. Treasury bills in Q1 2025, equal to roughly 1.6% of outstanding Treasury bills, making it one of the largest non-sovereign buyers in that market, and top 17th largest holder of U.S. debt globally.

Stablecoins are not just liquidity inside crypto. They are a bridge between offshore dollar demand, Treasury collateral, and on-chain settlement. If stablecoin supply expands, crypto gets more transactional liquidity and the Treasury gets another buyer. If stablecoin growth stalls, crypto loses one of its cleanest plumbing tailwinds.

Stablecoins have continued to grow even as 3-month bill yields have fallen, which suggests demand is not simply a yield-arbitrage trade. The GENIUS Act gives the sector a clearer U.S. regulatory framework, and Bessent has argued that stablecoins could grow roughly tenfold to around $3tn by 2030, creating a new source of demand for short-duration Treasuries. That makes stablecoins look less like offshore crypto plumbing and more like a structural dollar-liquidity rail: crypto gets a deeper liquidity base, while the Treasury gets another marginal buyer for bills.

Macro

Macro is also becoming less about the Fed meeting and more about the buyer of last resort.

The Fed still matters, but the long end is doing most of the talking. In May, global bond markets were hit by the Iran war, hotter inflation, and growing concern about public debt. The 30-year U.S. Treasury yield briefly reached around 5.2% on May 20, its highest level since 2007, before peace-talk hopes and softer growth data helped yields calm down.

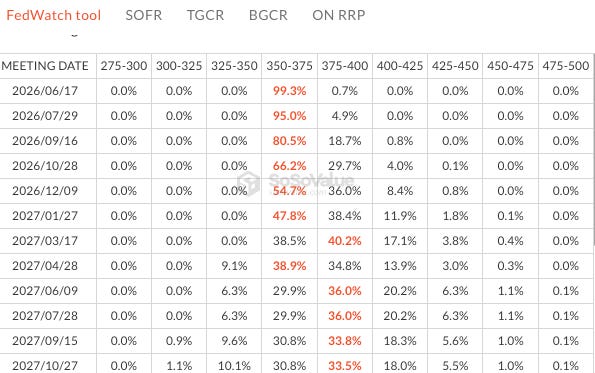

Market has repriced the potential of a fed hike again this week, currently looking for an unchanged trajectory for a longer period of time.

That is the macro regime in one paragraph. The market is not simply pricing inflation. It is pricing inflation plus supply plus fiscal risk plus uncertainty over who absorbs duration.

The fiscal numbers are not catastrophic day to day, but they are heavy enough to matter. The U.S. posted a $215 billion April surplus, which sounds fine until you notice it was down 17% from a year earlier, while outlays rose and gross interest on the public debt hit a record monthly $112 billion. For the first seven months of fiscal 2026, gross interest costs reached $734 billion, up $50 billion from the year before.

That is why the bond market is no longer treating deficits as background noise. Interest expense is becoming a flow. It is not just a spreadsheet problem for 2034. It is a monthly cash-flow item that has to be financed today.

Treasury borrowing also remains a live issue. The Treasury lifted its April-June borrowing estimate to $189 billion, $79 billion above its February projection, and projected $671 billion of borrowing in the July-September quarter. That does not mean the market cannot absorb it. It means absorption is now a price-sensitive process.

This is the part that connects directly to risk assets. When the government needs more buyers, when AI companies need more financing, when stablecoin issuers need more bills, and when investors can earn real yield in cash or Treasuries, every speculative asset has to compete harder for capital.

Inflation makes that competition worse. April PCE rose 3.8% year on year, the fastest pace since May 2023, while core PCE rose 3.3%. The monthly core number was less alarming at 0.2%, but the headline pressure still came through energy, with the Iran war and Hormuz disruption feeding directly into prices. Consumer spending rose, but the saving rate fell to 2.6%, and real disposable income weakened.

That is not a clean recession setup. It is also not a clean soft-landing setup. It is a nominal resilience setup. Households are still spending, AI capex is still running, government outlays are still large, but the financing cost of that resilience is going up.

This is why the market can rally on peace headlines and still feel fragile. A credible US-Iran deal would lower oil risk premium and help the inflation path. But it does not solve Treasury supply. It does not solve interest expense. It does not solve the fact that AI capex is competing for capital at the same time the government is issuing more debt.

The Collateral Trade

The theme this week is that the market is becoming a collateral trade.

That sounds abstract, but it is very practical. The assets that matter most right now are the ones that either create collateral, absorb collateral, or compete with collateral.

Treasuries are the base collateral. Stablecoins are becoming a new wrapper around short-duration Treasuries. BTC is trying to become pristine non-sovereign collateral. AI infrastructure is issuing claims on future productivity. Equities are claims on earnings. Altcoins are claims on future network value. All of them are competing for the same investor balance sheet.

In the zero-rate world, the market could buy all of them. In this world, it has to choose.

That is why dispersion should increase. The market will not simply buy “crypto” because regulation improves. It will buy the parts of crypto that improve the collateral stack. The market will not simply buy “AI” because capex is large. It will buy the parts of AI that own bottlenecks, power, grid access, memory, cooling, or financing channels. The market will not simply buy “risk” because oil falls. It will buy assets whose liquidity improves when oil falls.

BTC fits that world better than most crypto. Stablecoins fit it better than most DeFi tokens. Regulated derivatives venues fit it better than offshore leverage tokens. SOL can still outperform tactically, but structurally the market is moving toward collateral, settlement, and regulated leverage.

That is also why ETH needs to prove what it is. Is it money? Is it equity in the settlement layer? Is it yield-bearing internet collateral? The market is not giving full credit for all three at once anymore. It wants one clean answer.

[Chart 6: BTC market cap vs stablecoin supply vs Treasury bill issuance. Place at start of theme section.]

Looking Ahead

Next week, the question is not just whether BTC holds a level or whether the Fed sounds hawkish. The better question is whether balance sheet becomes easier or harder.

For crypto, watch three things medium term.

I. BTC performance while real yields stay elevated.

II. Stablecoin supply resumes growth rather than just staying flat.

III. Onshore perp story creates genuine liquidity or simply more regulated leverage in a market that is not ready to use it.

For macro, watch the long end more than the Fed speakers. If 30-year yields calm down and oil keeps falling, risk assets can breathe. If long-end yields rise even as oil falls, that is a much more important warning, because it would mean the issue is no longer just inflation. It would mean the market is pushing back on fiscal supply.

The bottom line is that this is not last week’s market anymore. The US-Iran deal still matters, but it is no longer the whole story. The deeper issue is absorption. Who buys the Treasuries? Who finances the AI buildout? Who holds the stablecoin collateral? Who warehouses crypto leverage? Who pays for duration?

In a market like this, the winners are not always the assets with the best story. They are the assets that can become part of the collateral system.